You Just Got a Term Sheet. Do Not Sign It Yet.

The complete Claude prompt system for reading every clause and walking into negotiations knowing exactly where to push

A term sheet arrived in your inbox. It looks short. Maybe eight pages. Maybe one. There is a valuation on it that makes you feel something. And there is a clock running you cannot see.

Here is what most first-time founders do not know: the valuation is not the term sheet. The valuation is the number that keeps you distracted while the actual deal terms are written around it. The liquidation preference, the option pool, the anti-dilution clause, the board seat, the no-shop window: these are the terms that will determine how much money you actually make when you exit. And they are all negotiable before you sign. None of them are negotiable after.

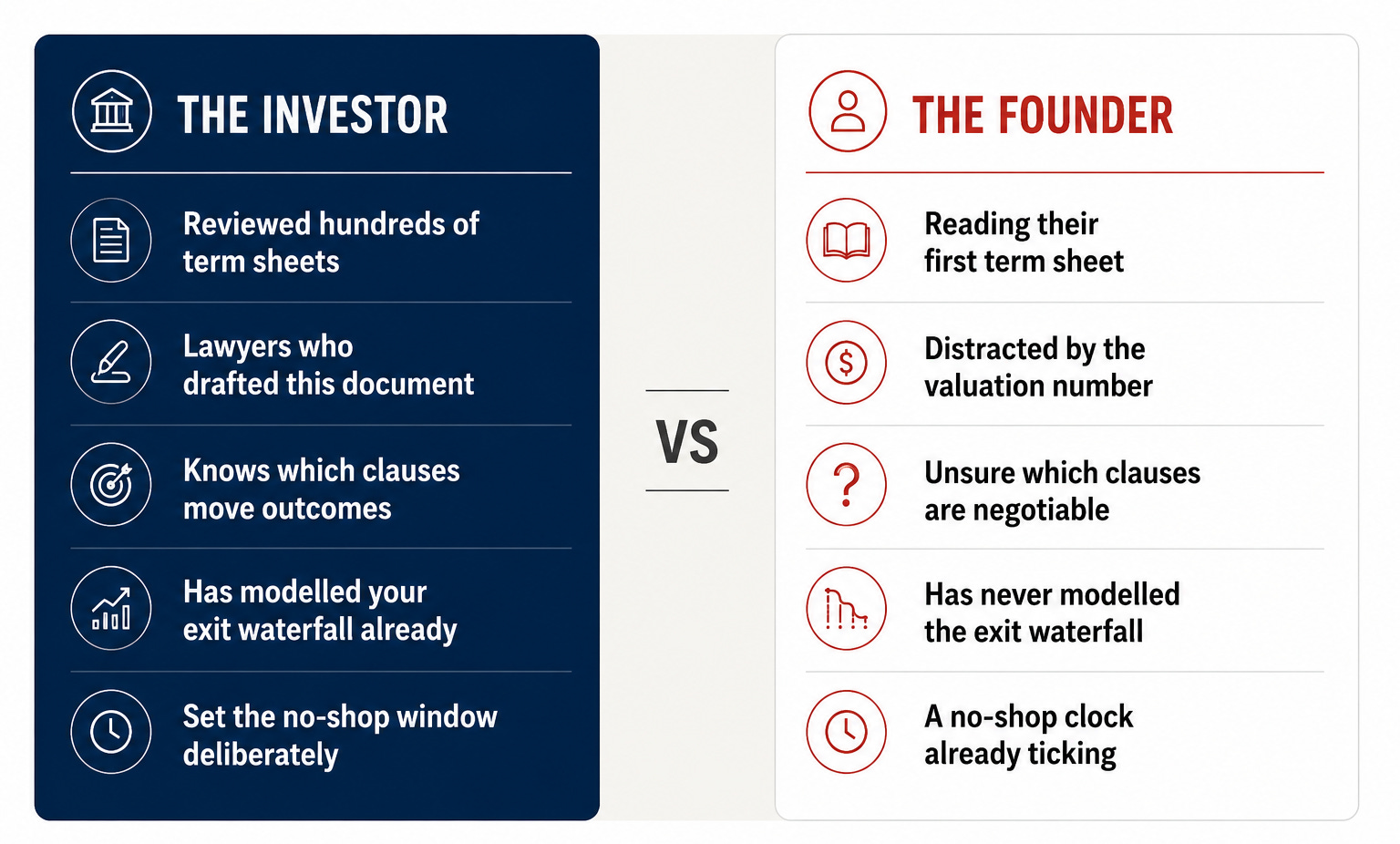

The problem is that you have probably never read a term sheet before. You are sitting across the table from a firm whose partners have reviewed hundreds of them. They have lawyers who drafted it. You have 72 hours, a no-shop clause ticking, and a lawyer you are not sure you can afford to call at this hour.

This article gives you the Claude prompt system to change that dynamic. Not to replace your lawyer. But to make sure that by the time you get on the phone with them, you already know what you are looking at.

What investors know about your term sheet that you probably do not

Let us start with the data, because it reframes everything.

Three numbers to hold onto:

Those numbers tell you something important. The headline economics are now so standard that if your term sheet says anything else, you should treat it as a red flag, not a starting point for negotiation. But the governance terms, the veto rights, the board structure, the option pool placement: these are where deals quietly tilt away from founders, and where almost every term sheet has room to move.

That last point is the one most founders miss entirely. When an investor says they want a 15% option pool, what they often mean is they want a 15% pool created before their investment is counted, in the pre-money valuation. That pool dilutes you, not them. On a £5M round at a £20M pre-money, the difference between a pre-money and post-money option pool is worth around £750,000 in founder equity. Claude can model this for you in about 30 seconds. Your lawyer would charge you £300 to explain it.

Note on the data: Term sheets are becoming more investor-friendly again. HSBC Innovation Banking’s 2025 analysis of 588 signed UK term sheets found that participating preferences, while becoming less common at Series B and above, are rising at seed. Pay-to-play clauses are at their highest in Cooley’s recorded US history. The market is not as founder-friendly as 2021. Know what you are reading.

The five clauses that actually determine your exit outcome

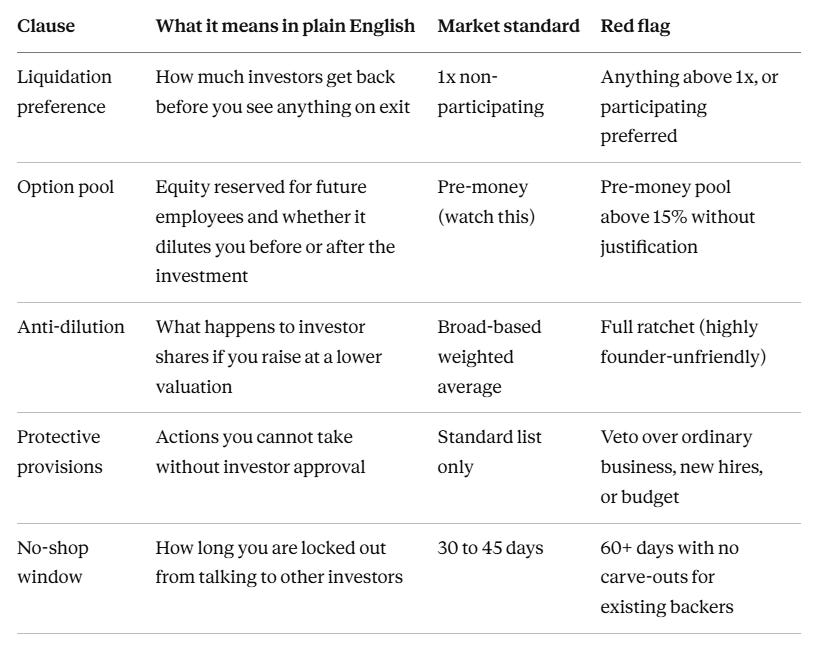

Before we get to the prompts, you need to understand the five terms that will determine how much money you walk away with when your company exits. Everything else is context. These are the economics.

Prompt 01: The Plain English Decoder

Paste your full term sheet into Claude and run this. Every clause, translated.

I have just received a term sheet and I need you to help me understand it clause by clause. I am a founder and this may be my first term sheet. Do not use legal jargon. For each major clause:

1. Explain what it means in plain English (2 to 3 sentences maximum)

2. Tell me whether this is standard, above market, or a red flag based on current 2025 market practice

3. If it is a red flag, tell me specifically why and what I should push back on

4. If it is above market in my favour, tell me so I can identify my leverage points

Use the following benchmarks:

- Liquidation preference: 1x non-participating is standard. 2x or participating is a red flag.

- Option pool: post-money creation is better for founders. Pre-money above 15% is worth questioning.

- Anti-dilution: broad-based weighted average is standard. Full ratchet is a red flag.

- No-shop: 30 to 45 days is standard. 60+ days with no carve-outs is above market for investors.

- Pay-to-play: present in roughly 10% of US deals (Cooley Q2 2025). Not standard. Push back.

- Board seats: one investor board seat is standard at Seed. Two is above market for investors.

After the full clause-by-clause breakdown, give me:

- A summary of the three clauses I should prioritise in negotiation

- A summary of the clauses I should accept without pushback

- An overall assessment: is this term sheet founder-friendly, market-standard, or investor-friendly?

Here is my term sheet:

[PASTE YOUR FULL TERM SHEET HERE]Prompt 02: The Exit Waterfall Model

This shows you what you actually take home at different exit valuations. Not what you think you will take home. What you actually will.

On the same exit, the difference between standard and dirty terms can cost founders millions. A 2x participating preference on a £30M exit at a £25M post-money valuation costs founders roughly £10M compared to 1x non-participating terms. The investor doubled their money either way. Claude’s waterfall model makes this visible in 30 seconds.

I want you to build an exit waterfall model for me based on the following term sheet terms. Show me what each party receives at five different exit valuations.

Investment amount: [£X]

Pre-money valuation: [£X]

Post-money valuation: [£X (pre-money + investment)]

Liquidation preference: [1x / 1.5x / 2x]

Participation: [non-participating / participating / capped participating at Xx]

Option pool size: [X%]

Option pool timing: [pre-money / post-money]

Investor ownership post-close: [X%]

Founder ownership post-close (after option pool dilution): [X%]

Run the waterfall at these five exit valuations:

- 0.5x the post-money valuation (acqui-hire / distressed exit)

- 1x the post-money valuation (flat exit)

- 2x the post-money valuation (modest return)

- 5x the post-money valuation (strong return)

- 10x the post-money valuation (exceptional outcome)

For each scenario, show:

1. How much the investor receives

2. How much common shareholders (founders + employees) receive collectively

3. Founder's approximate share of that common pool assuming [X%] personal ownership

4. The breakeven exit valuation where I start receiving anything meaningful

Also: if my term sheet has a participating liquidation preference, show me the same waterfall with a standard 1x non-participating preference instead, so I can see the cost to me in pounds at each exit scenario.

Format this as a clear table I can share with my co-founder and lawyer.If you are raising in the next six months, these are the articles that will do the most work alongside this one.

→ The Quiet Filter That Decides Your Entire Fundraise - the investor screening process most founders never see, and how to make sure you pass it

→ The Number That Kills More Fundraises Than Any Bad Idea - the market size mistake costing founders millions in missed funding

→ The Most Dangerous Document a Founder Will Ever Sign - The term sheet clause quietly stripping founders of control

The first two prompts decode what you have and model your real numbers. The five prompts below build what most founders never prepare - and what separates the ones who negotiate from the ones who sign and regret.

What’s inside:

✅ Prompt 03: The Negotiation Brief - clause by clause, tells you what to push back on, what to concede, and writes the opening email that starts the conversation without damaging the relationship

✅ Prompt 04: The IP Clause Scanner - reviews every provision that touches your intellectual property and tells you exactly what risk each one creates and what language to request instead

✅ Prompt 05: The Protective Provisions Audit - categorises every investor veto right as standard, watch, or push back, and drafts the paragraph you send to narrow the ones that matter

✅ Prompt 06: The Board Dynamics Simulator - runs your proposed board structure through three scenarios and tells you who actually controls the company when things get hard

✅ Prompt 07: The No-Shop Countdown Brief - builds your complete timeline from signing to close, the diligence checklist to prepare in advance, and the early warning signals that the deal is slowing down

This is what a paid subscription to The Founders Corner gets you every week.

Not frameworks to screenshot and store. 50+ tools you open, use, and walk away from with something concrete, built for the decisions founders are actually making.

Prompts 03 through 07 are available exclusively to premium subscribers of The Founders Corner.

Prompt 03: The Negotiation Brief

Keep reading with a 7-day free trial

Subscribe to The Founders Corner® to keep reading this post and get 7 days of free access to the full post archives.