The Call Your Investor Wants You to Take Unprepared

Most founders say yes before they understand what they are agreeing to.

The email arrives from your lead investor on a Tuesday morning.

“We’ve been thinking about your next round. We’d love to lead it ourselves. Let’s get on a call.”

For most founders, this feels like the best possible news. Your investor is in. You do not have to spend six months fundraising. You can focus on the business.

Do not say yes yet.

What just arrived in your inbox is not an offer. It is the opening move of a negotiation you are probably not prepared for. The terms embedded in it will determine what you take home when the company eventually exits.

Most founders sign insider-led rounds without understanding what they agreed to. They find out what it meant three or four years later, in a room with a banker and a spreadsheet, when the numbers do not add up the way they expected.

This piece is about what to do before that call.

What the Insider Round Actually Is

An insider-led round is a funding round led primarily or entirely by your existing investors, without a new lead investor setting the price.

It sounds simple. It is not.

In a normal externally-led round, a new investor does price discovery. They look at the market, at your metrics, at comparable companies, and they set a valuation that reflects what an independent party believes the business is worth. That valuation is the foundation for everything that follows: your option pool, your employee equity, your liquidation stack, your next raise.

In an insider-led round, your existing investor sets the valuation. They are not an independent party. They have information advantages you are not aware of. They know what they paid in the last round. They know what your cap table looks like. They know exactly what terms they want. And they know you are unlikely to have run a parallel process before taking the call.

This is not a reason to refuse the insider offer. It is a reason to understand exactly what you are agreeing to before you agree to it.

Why Investors Offer to Lead Insider Rounds

There are four versions of the insider offer. They look identical from the outside.

Genuine conviction. Your investor believes the next round will be significantly more expensive. They want to buy now at the current valuation before an outside investor prices a higher round. This is the best version of the offer. You should still negotiate every term.

Portfolio mechanics. Most VC funds have pro-rata rights, which give them the right to maintain their ownership percentage in future rounds. The offer to lead may be driven by fund mechanics rather than genuine enthusiasm for the business at this specific stage.

A market signal they are managing. Internal bridge rounds do not require public disclosure. If your investor doubts you will get outside terms, leading the round themselves avoids the public signal of a difficult raise. This is the version that requires the most caution.

Relationship preservation. Some investors lead insider rounds because they believe the relationship matters more than the economics of this particular round. They want to demonstrate ongoing support to the team and to the market.

The question is which version you are looking at. The answer changes everything.

Here is how to find out. Ask them to introduce you to three outside investors before you accept their terms. Their willingness to do so tells you more than anything they say in the call.

The Signalling Risk Nobody Warns You About

The insider-led round is the most misunderstood signalling event in start up fundraising.

When your next raise begins, every sophisticated investor will ask the same question: why did your existing investor lead the last round?

If the honest answer is that you could not find an external lead, that conversation is starting from a position of weakness. The investor is not just pricing your current round. They are pricing the question of why an independent party was not willing to set that price.

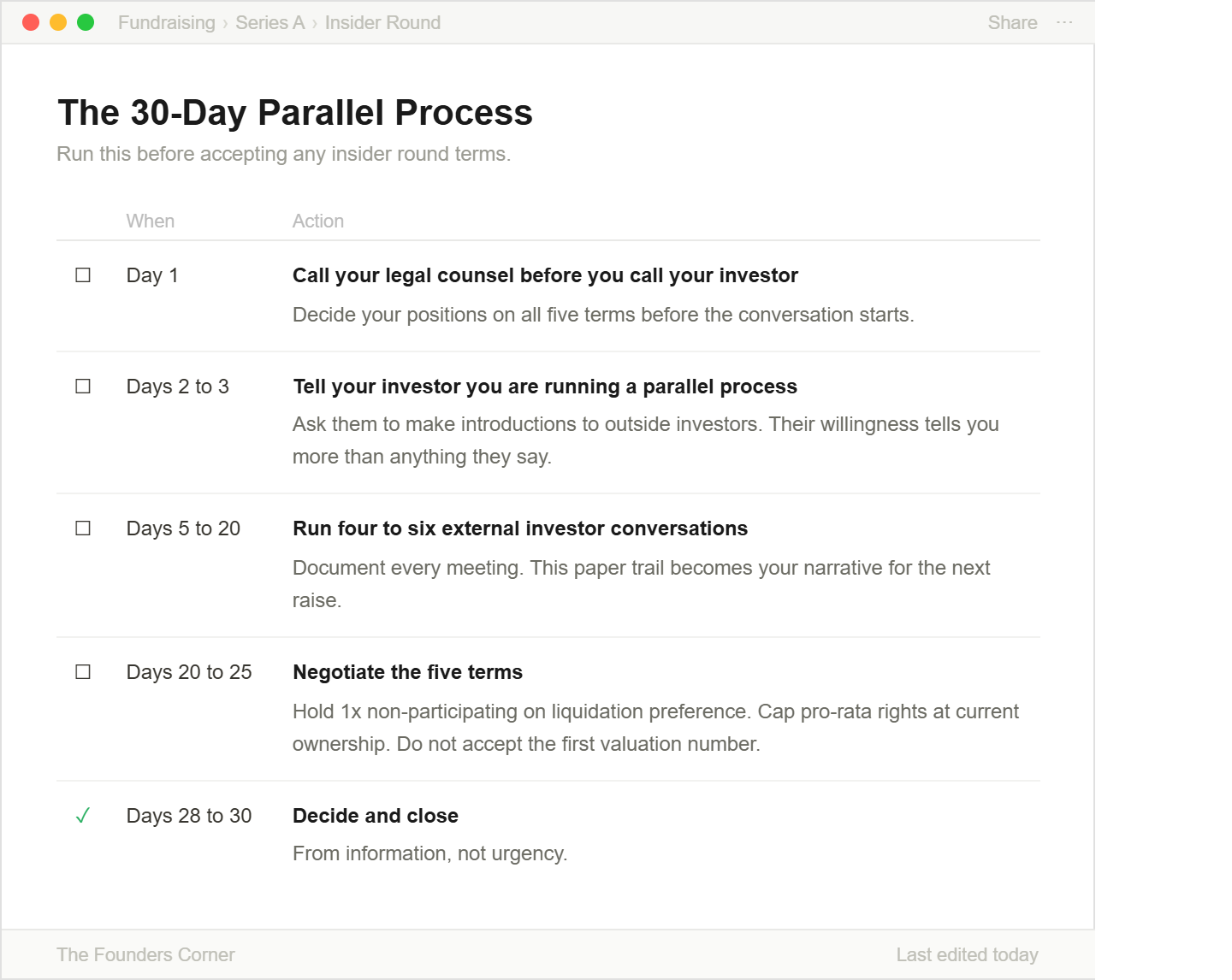

The founders who navigate this successfully do one thing before accepting insider terms: they run a genuine parallel process. Not performative conversations. Real ones. Four to six outside investors. Actual term sheet conversations where possible. Documented feedback.

That paper trail becomes your narrative. We had options. We had external interest. We chose to stay with our existing relationship because of domain expertise and track record. That is a story the next investor can believe. The alternative is not.

The Five Terms That Determine What This Round Actually Means

Most founders negotiate the valuation. Sophisticated founders negotiate all five of these.

1. Valuation. The valuation your insider sets anchors every future raise. A low insider valuation is not just a bridge. It is the reference point every new investor will start from. Push for a valuation that reflects your last twelve months of operational progress. Use recent comparable transactions as anchors. Do not accept the first number.

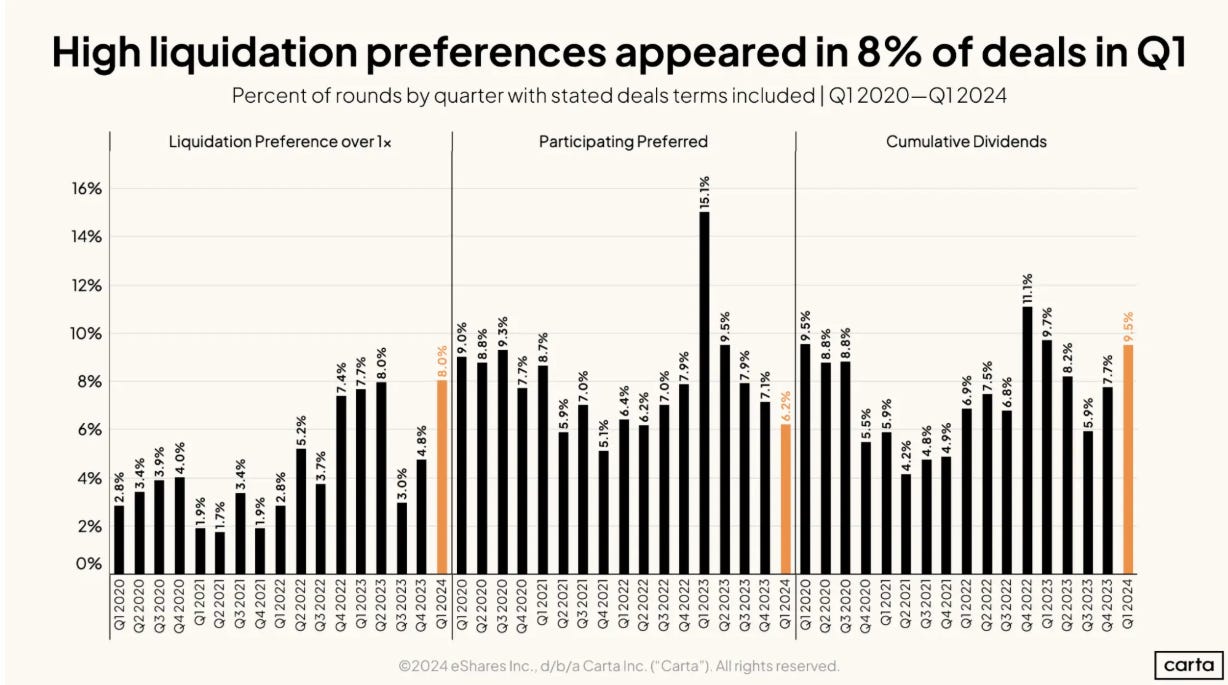

2. Liquidation preference. This is the one that costs founders the most money and gets the least attention.

Standard is 1x non-participating. This means that in the event of an exit, your investor gets back 1x their investment before anything flows to common shareholders. At a strong exit, they convert to equity and participate on the same basis as everyone else. This is clean and founder-friendly.

A 2x liquidation preference on a £5M round means your investor takes the first £10M from any exit before founders or employees receive anything. At a £15M acquisition, which looks like a success from the outside, your team receives nothing if the investor chooses to take their preference.

Hold the line at 1x non-participating. If they push above 1x, ask what specific risk they are pricing. Then address that risk directly. Do not simply accept a higher multiple because the conversation is uncomfortable.

3. Pro-rata rights in the next round. If your investor takes pro-rata rights to follow on in the next round, they can claim a significant slice of your next raise before you fill it with new relationships. Super pro-rata rights, which give them the right to increase their percentage, can effectively pre-allocate your next round before you begin the process. Cap pro-rata rights at their current ownership percentage. Resist super pro-rata in any form.

4. Pay-to-play provisions. A pay-to-play clause requires all existing investors to participate in the current round or lose rights in future ones. It can be a legitimate tool to consolidate the cap table. It can also be a mechanism to squeeze out earlier investors who do not have the reserves to participate. Before agreeing, model the exact impact on each existing investor on your cap table. Surprises here damage relationships that matter.

5. Board composition. Insider-led rounds sometimes come with requests for additional board seats or observer rights. An expanded board at this stage is harder to restructure later. Protect your independent board seat. If they want an additional seat, negotiate for an independent director of your choosing to balance the composition.

If you are navigating a funding round in the next 60 days, these are the issues that will do the most work alongside this one.

→ The Most Dangerous Document a Founder Will Ever Sign - the full term sheet deep dive, the clauses that matter most and the ones that follow you for years. Read this before you sign anything.

→ Before You Pitch: The Negotiation Secrets Investors Don’t Want You to Know -how to enter any funding conversation with leverage rather than gratitude.

→ The Data Room That Closes Deals - what to send, how to structure it, and the 10-minute audit to run before every send.

The Exit Waterfall Most Founders Never Run

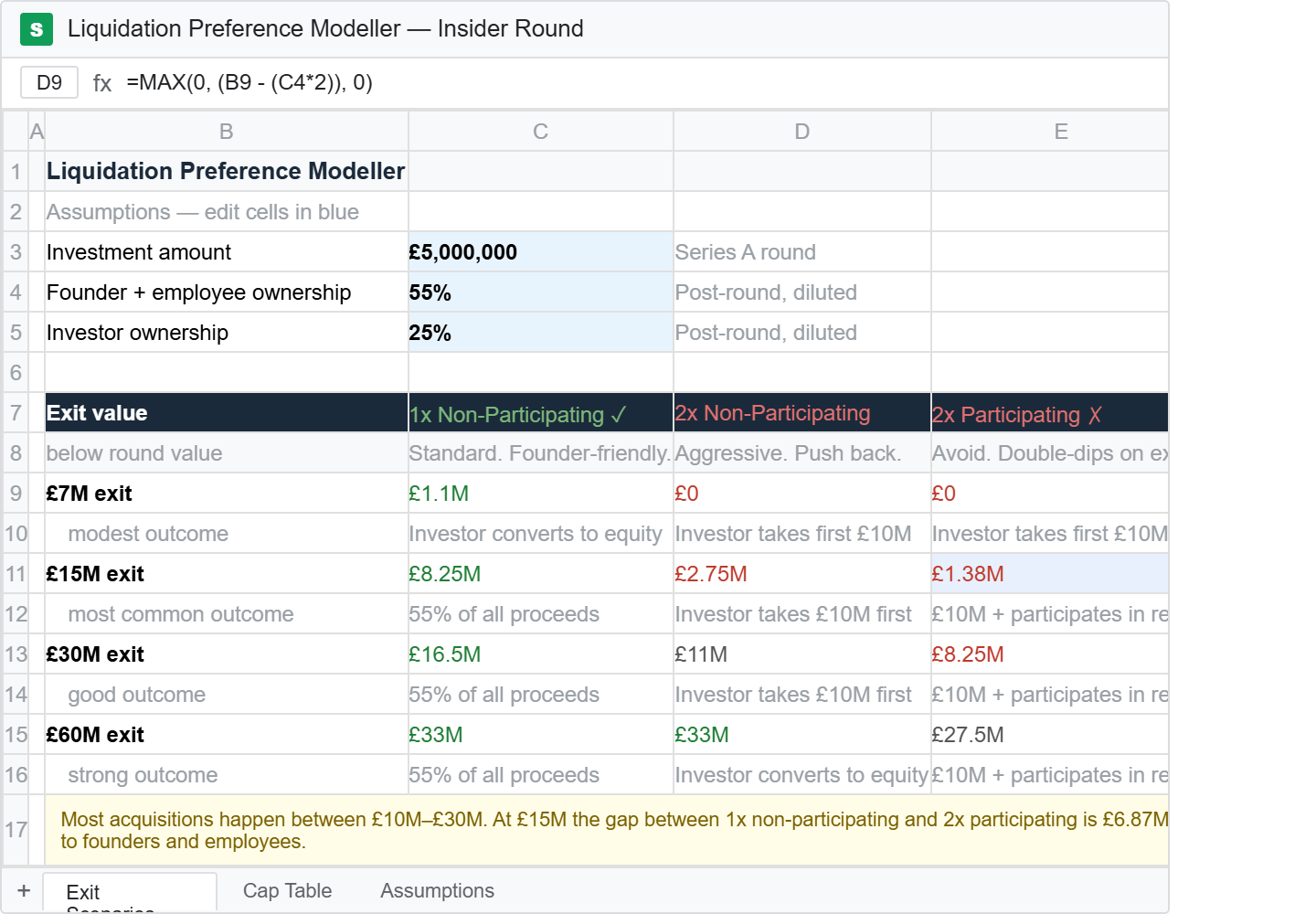

Before you negotiate a single term, run this exercise.

Take the proposed investment amount. Take the proposed valuation. Take the liquidation preference they are asking for. Then model what you and your team receive at three exit valuations: the current round valuation, 2x the current round, and 0.75x the current round.

Most founders are surprised by what they find at the 0.75x scenario. An acquisition at a flat or modest valuation, which represents the most common start-up outcome, distributes very differently depending on whether the preference is 1x or 2x, participating or non-participating.

Participating liquidation preference is far more aggressive and can seriously reduce common shareholders’ pay-outs. That is why it is a red flag in any term sheet.

How to Have the Parallel Process Conversation

The most effective thing a founder can do when they receive an insider offer is to tell their investor they plan to run a parallel process.

Most founders avoid this conversation because they are afraid of damaging the relationship. It does not damage it. Done correctly, it protects it.

The conversation is straightforward.

“We are genuinely excited about your continued support and we want to move quickly. We are also going to spend the next thirty days having a small number of conversations with outside investors. Not to replace you. To ensure we understand the market and give you confidence that the valuation we agree on is the right one. Would you be willing to make two or three introductions to funds you think should see this?”

An investor who is confident in the business and confident in the terms they are offering should welcome this. An investor who resists it is telling you something.

The parallel process is not a negotiating tactic. It is how you build the evidence that this was a choice. Evidence you will need when the next investor asks why you did not go to market.

The Conversation to Have Before the Term Sheet Arrives

The terms of insider rounds are often agreed in conversation before anything is written down. By the time a term sheet arrives, both sides have usually established a working understanding that is difficult to renegotiate.

This means the most important negotiating moment is the call you have not yet taken.

Before that call, decide your positions on each of the five terms. Write them down. Discuss them with your co-founders. Call your legal counsel. Understand your walk-away points.

Then, in the call, when your investor says “we’re thinking 1x participating preferred,” a real ask that is becoming more common, you will know immediately why that matters and what to say.

The insider round is not a threat. Your investor offering to lead is, in most cases, a genuine signal of commitment to the company. The best investor relationships are ones where both sides can negotiate honestly, know what they are agreeing to, and build terms they can both explain to the next person who asks.

That is the outcome to aim for.

Not the fastest close. Not the most harmonious call.

The terms that are fair, the narrative that holds up, and the cap table that does not require explaining at the next raise.

The Insider Round Negotiation Playbook

The Insider Round Negotiation Playbook is a five-section document built from the exact framework I use when preparing portfolio founders to respond to insider offers.

It is not a summary. It is not a checklist you glance at once and close. It is the document you open before you take the call, work through section by section, and return to before you sign anything.

What’s inside:

✅ Why Insiders Lead - the four versions of the insider offer, how to identify which one you are looking at, and what to ask before you respond

✅ The Five Terms That Matter - valuation, liquidation preference, pro-rata rights, pay-to-play, and board composition, with exactly what to negotiate for on each one

✅ The Signalling Risk - how to manage market perception so the insider round becomes a strength in your next raise, not a liability

✅ The Negotiation Checklist - every conversation to have, every term to review, and the red lines to hold, from before you respond to after you close

✅ The Liquidation Preference Modeller - enter your numbers and see what each preference structure means for founders and employees at three different exit valuations

This is what a paid subscription to The Founders Corner gets you every week.

Not frameworks to screenshot and store. 50+ tools you open, use, and walk away from with something concrete, built for the decisions founders are actually making.

The Playbook is available exclusively to premium subscribers of The Founders Corner.

Download The Playbook

Keep reading with a 7-day free trial

Subscribe to The Founders Corner® to keep reading this post and get 7 days of free access to the full post archives.