The Data Room That Doesn’t Lose Deals at the Last Minute

Founders spend months getting to term sheet. Then lose the deal in the data room. Here is how to prevent it.

It is 9:47 PM on a Tuesday. The term sheet was signed eleven days ago.

The Slack message arrives from the lead partner. “Quick one. Can you reconcile the ARR in the deck with the trailing twelve in the model? We’re seeing a $1.4M gap and the team needs it cleared before IC tomorrow.”

The founder opens both files. The deck says $14.2M ARR. The model shows $12.8M. They are supposed to be the same number.

They aren’t. Not because the founder is dishonest, but because the deck includes annualised MRR from contracts signed last week that have not yet billed, and the model uses recognised revenue. Two legitimate definitions. One catastrophic gap.

The deal does not die that night. It dies six days later, after three more inconsistencies surface, each one reasonable in isolation, all of them together fatal.

This is not a story about a bad business. The company had real revenue, real growth, and real customers. It is a story about a data room that did the founder’s thinking against them.

Between 15% and 25% of signed term sheets and LOIs do not close. The failures almost never trace back to the business fundamentals. They trace back to discoveries during diligence that a prepared founder could have resolved in advance.

Bain’s most recent global M&A research found that more than 60% of executives cite poor diligence preparation as the primary driver of deal failure. Sprinto’s 2025 review of deal collapses concluded that nearly half of all deals fall apart during due diligence, most often when investors find liabilities the founders had overlooked or quietly downplayed.

These are not negotiating chips. They are deal-stoppers an investor uses to justify a decision they have already started drifting toward, or that genuinely recalibrate their view of the business.

This is how you prevent it.

The misconception that kills deals

Most founders treat the data room as a filing cabinet. A place to upload the documents an investor asks for, organised the way the founder thinks about their business.

This is exactly backwards.

The investor’s diligence process does not move through your business in the order you built it. It moves through six predictable categories, in a predictable sequence, run by people whose job is to find reasons not to invest.

Build for the order they actually move in. Not the order you wish they would.

Here is the sequence. Memorise it.

▫️ Days 1-3: Cap table and corporate

▫️ Days 3-10: Financial reconciliation

▫️ Days 10-15: Customer and commercial

▫️ Days 15-21: Legal, IP, and HR

▫️ Days 21-28: The disclosure schedule

Investors form impressions in order. By the time they reach commercial diligence, they have already decided whether your numbers are credible. By the time they reach legal, they have already decided whether to trust the team. The first 72 hours of your data room either build trust or burn it.

The rest of diligence is then conducted in the shadow of that early impression.

The three categories of data room problem

Almost every late-stage deal collapse traces back to one of three categories. The names matter because they tell you where to look.

1. Financial inconsistency

The most common deal-killer is not bad financials. It is contradictory financials.

ARR in the deck. Bookings in the model. Recognised revenue in the audit. Three numbers that should bridge cleanly but rarely do. Founders treat them as interchangeable. Investors treat them as three different facts.

The fix is a bridge document. One page that shows how booked revenue converts to billings, billings to recognised revenue, recognised revenue to GAAP. Preparing the bridge surfaces the inconsistencies you would otherwise not catch until the investor catches them.

Other common financial traps:

▫️ Burn rate that differs across documents. If your deck says you are burning $400k a month and your model implies $520k, that is a credibility-destroying gap. Reconcile both to the bank statements.

▫️ CAC that is suspiciously clean. Blended CAC hides everything. Investors will rebuild it by channel. Hand them the data first, with the worst channel circled. Self-disclosure inverts the dynamic.

▫️ Cohort analysis that arrives late. If you do not provide net revenue retention by cohort, the investor will rebuild it from raw data. Their version will be less generous than yours.

2. Legal incompleteness

This is the category founders most underestimate. The product is real. The traction is real. The cap table looks fine. Then somewhere on day eighteen, the investor’s counsel finds the issue that ends the conversation.

The most common legal landmines:

▫️ The 83(b) election that was never filed. When founder stock is issued subject to vesting, the founder has 30 days to file an 83(b) with the IRS. Miss the deadline and every vested tranche becomes ordinary income at the new round’s valuation. The founder owes tax on shares they cannot sell.

election form used by startup founders receiving restricted stock, illustrating the legal and tax filing that must be submitted within 30 days to avoid future diligence issues.")

▫️ The cap table that does not reconcile. The deck says one ownership number, Carta says another, the board consents reference a different option pool. Every diligence team finds at least one of these. The fix is mechanical: tie every share, every SAFE, every option grant back to a board consent, eight weeks before raising.

▫️ The IP assignment that was never signed. Every employee, contractor, advisor, and weekend volunteer who touched the product must have signed an IP assignment. The freelance designer from year one. The friend who wrote the original API. If they did not sign, the company does not own its own product.

▫️ The change-of-control clause in your top customer’s contract. A surprising number of enterprise contracts terminate automatically on equity events. Your largest customer’s contract becomes void the moment the round closes. Read every top-20 contract for change-of-control, assignment, and termination provisions. Get waivers in writing before diligence starts.

3. Business model red flags

These are the discoveries that do not technically end the deal but recalibrate the investor’s view enough to justify a re-trade or a walk.

▫️ Customer concentration above 20%. If a single customer is more than 20% of revenue, the investor is partly underwriting that customer. Above 30%, many funds will not proceed at all.

▫️ Pipeline that does not survive a reference call. Investors call your pipeline customers. They ask whether the customer is actually evaluating, what they would pay, when they would buy. Pipeline stages that look great on the dashboard often look very different on the call.

▫️ Churn without reason codes. A churn rate is a number. A churn rate with categorised reasons is a learning company. Investors view the second as fundable and the first as a guess.

▫️ Net revenue retention below 100% at any meaningful scale. This is a thesis-breaker for SaaS. If your NRR is not above 100%, do not pretend it is. Address it directly: the cohort, the cause, the fix.

The five documents that kill the most deals

Every diligence process is unique. But five documents show up again and again as the proximate cause of deal failure

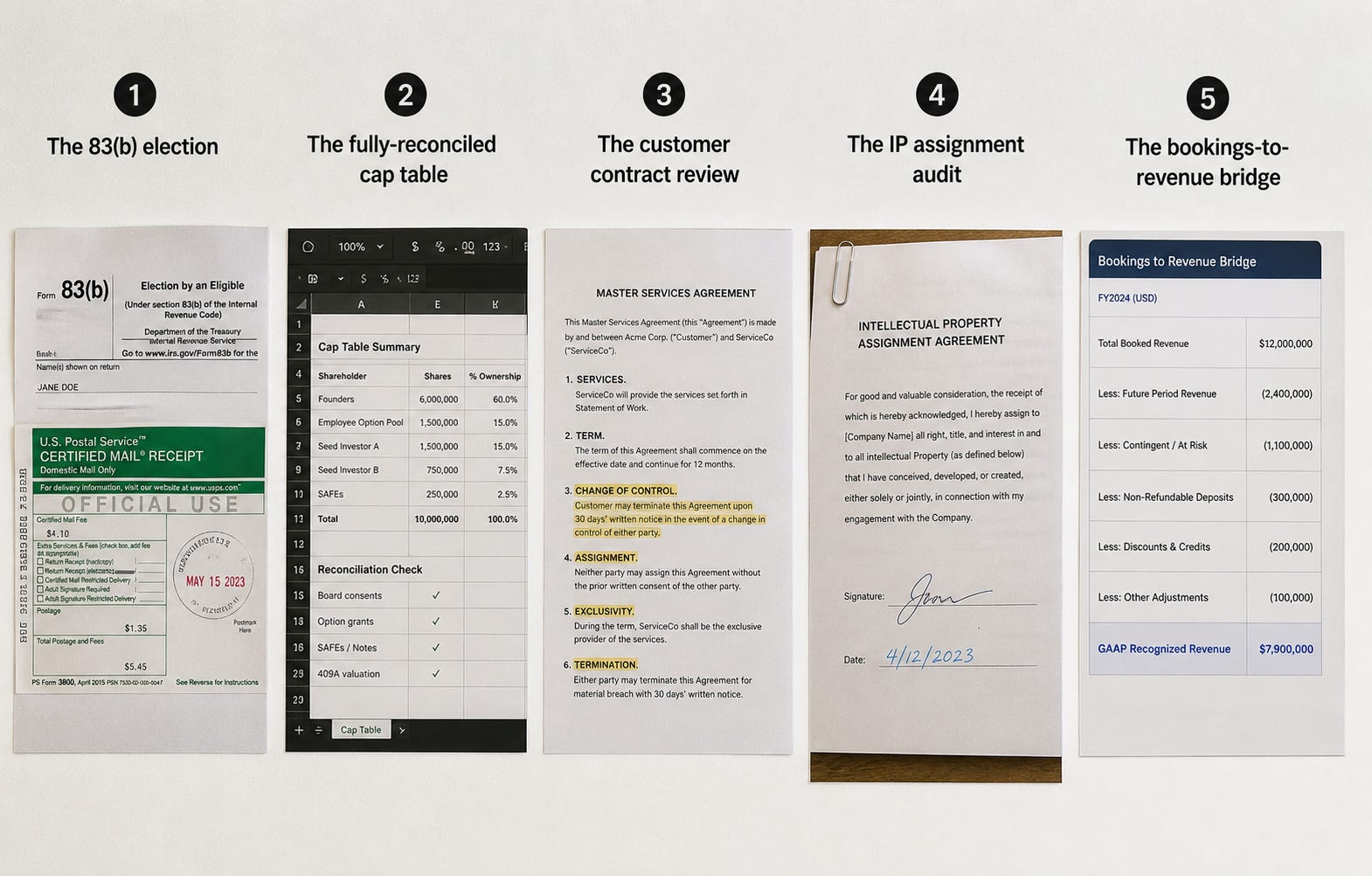

1. The 83(b) election

The single most common item that delays closing. Pull every founder’s 83(b) and confirm both the filing date and proof of mailing. USPS certified receipt is the gold standard. If a founder cannot produce one, work with a tax attorney immediately. Remediation paths exist but they take weeks and cost more the closer you get to the close.

2. The fully-reconciled cap table

Run a full reconciliation eight weeks before raising. Use Carta or Pulley’s built-in reconciliation report if available. Tie every share to a board consent. Investors do not just check that the percentages add to 100. They check that every grant has a corresponding consent, every SAFE has a signed agreement, every option grant references a valid 409A.

3. The customer contract review

Have counsel read every top-20 customer contract. The four clauses that matter most: change-of-control, assignment, exclusivity, and termination. Where issues exist, get a written waiver from the customer in advance. The investor will require this anyway. Better you ask than they do.

4. The IP assignment audit

Audit every contributor in the company’s history. Employees, contractors, advisors, anyone who touched the product. Where there is no signed IP assignment, get a confirmatory one now. Some former contractors will charge for this. Pay it. The alternative is the deal dying or your IP being unclear at exit.

5. The bookings-to-revenue bridge

The single document that prevents more deal collapses than any other. One page. Booked revenue at the top, GAAP-recognised revenue at the bottom. Every adjustment between them named and quantified. Put it in the data room before they ask.

The frame to take with you

Most founders build their data room to be comprehensive. The best data rooms are not comprehensive. They are pre-emptive.

A comprehensive data room contains everything an investor might want. A pre-emptive data room is built for the questions an investor will ask, in the order they will ask them, with the reconciliations and bridges already done.

The difference is the difference between an investor closing the room with no open questions and one closing it with three. The second investor takes those three questions to their partner meeting. The questions you leave open are the reasons your deal does not close.

Build the room the way diligence will work through it, not the way you organise information for yourself. Six folders, in the order partners actually read.

Then, the day before you send the link, walk through it as if you are the investor seeing it for the first time. The questions you find yourself asking are the questions they will ask.

Resolve them now. Not in week three of diligence, when momentum is the only thing keeping the deal alive.

📥 Get the Complete Data Room Construction Playbook

This guide gave you the categories. The Playbook gives you the execution.

Below is the full Data Room Construction Playbook. The asset that turns the principles above into a closeable diligence room.

What’s inside:

✅ The complete 47-item checklist organised by diligence category (Corporate & Legal, Financial, Commercial, Team & HR, IP & Technical, Operations & Risk)

✅ For every item: what investors are actually checking for and what makes a clean version of the document

✅ The five most common deal-killer documents with a pre-diligence resolution guide for each

✅ The investor-perspective walkthrough that maps how a partner moves through your room day by day, so you know which folders matter most in the first 72 hours

✅ A printable, fillable checklist your team can run through eight weeks before raising

This is the work that separates founders who close from founders who get re-traded.

The Playbook is available exclusively to premium subscribers of The Founders Corner.

The Data Room Construction Playbook

Keep reading with a 7-day free trial

Subscribe to The Founders Corner® to keep reading this post and get 7 days of free access to the full post archives.