Your Data Room Is Killing Your Round. Six Prompts to Fix It

Most founders send the data room link before they are ready. By the time they find out, the investor has already moved on

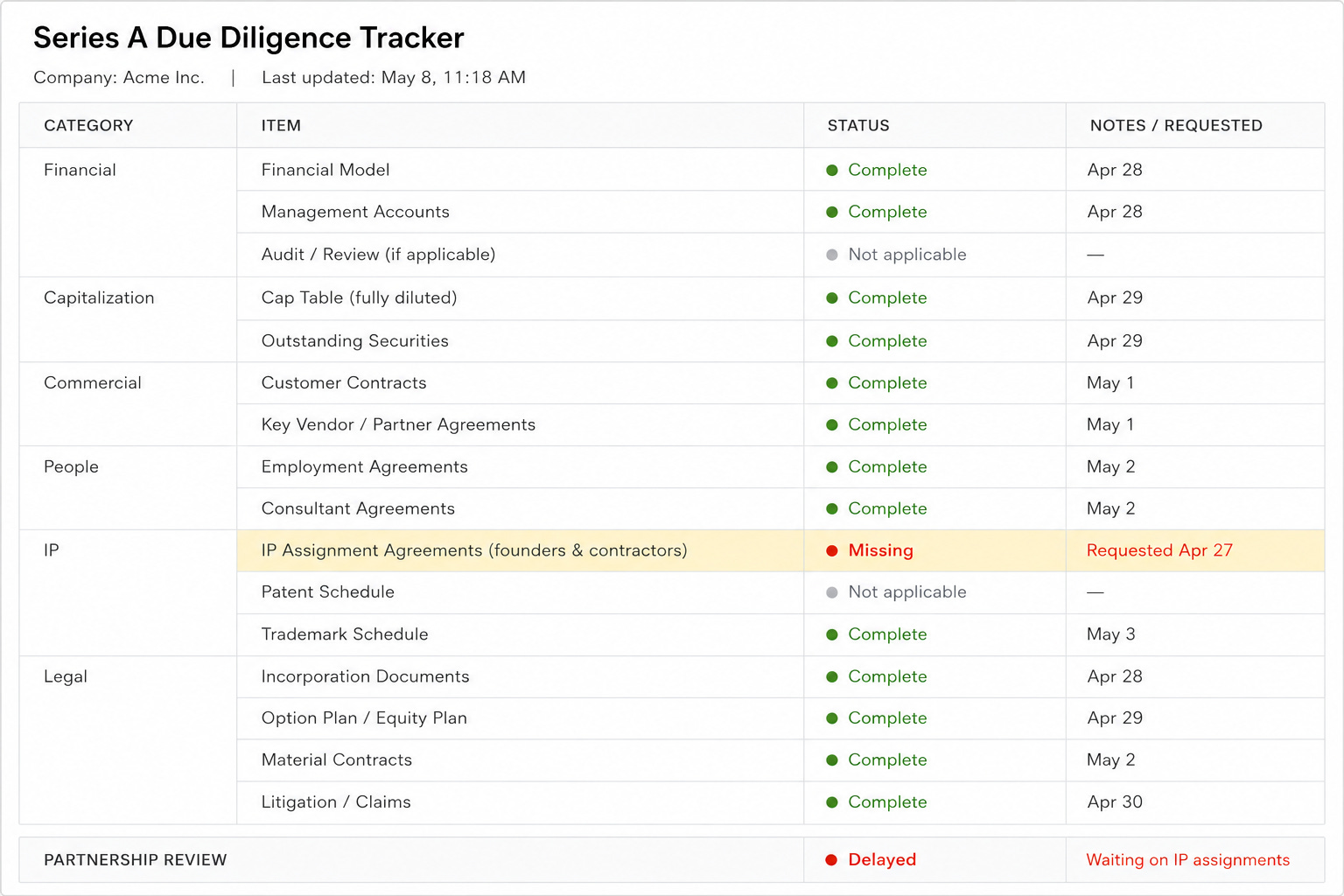

A founder I know had three co-founders and three early contractors. None of them had signed IP assignment agreements. Nobody had flagged it because nobody had asked and the founder had not thought to check.

The VC’s legal team opened the data room and found it in week one. The founder spent the next six weeks tracking down a former contractor who had moved to another country. The original term sheet expired. The lead investor walked.

They eventually raised. At a lower valuation. Six months late. Over one document that would have taken twenty minutes to prepare.

That story is not unusual. It is common.

The deal had been won in the pitch room and lost in the data room. Not because of anything wrong with the business. Because the documentation was not ready.

What the Data Room Is Actually For

Most founders treat the data room as an afterthought. A place to upload what the investor asks for, organised in the order things were built.

This is exactly backwards.

The investor’s diligence process does not move through your business in the order you built it. It follows a fixed sequence. The first 72 hours are where impressions and decisions are formed. Get that window right and everything that follows is interpreted charitably. Get it wrong and the investor spends the rest of the review looking for reasons to confirm their concern.

Investors see your data room as a preview of how you will run a company. If you cannot organise ten documents, how will you manage a team, a budget, or a product roadmap. That is not harsh. That is the actual mental model investors use during early-stage diligence. The document structure, the naming conventions, and what is missing all send signals about the founder’s operational maturity. Signals that are hard to reverse once formed.

The Numbers That Should Worry You

Half of all deals that reach term sheet still collapse during diligence. That is the number that matters. The pitch won the battle. The data room loses the war.

Most of those failures do not trace back to the business fundamentals. They trace back to documentation that was not ready, numbers that did not reconcile, and legal gaps the founder did not know existed.

How Investors Actually Read a Data Room

Most founders imagine due diligence as a patient, document-by-document review. An investor reading everything before forming a view.

That is not how it works.

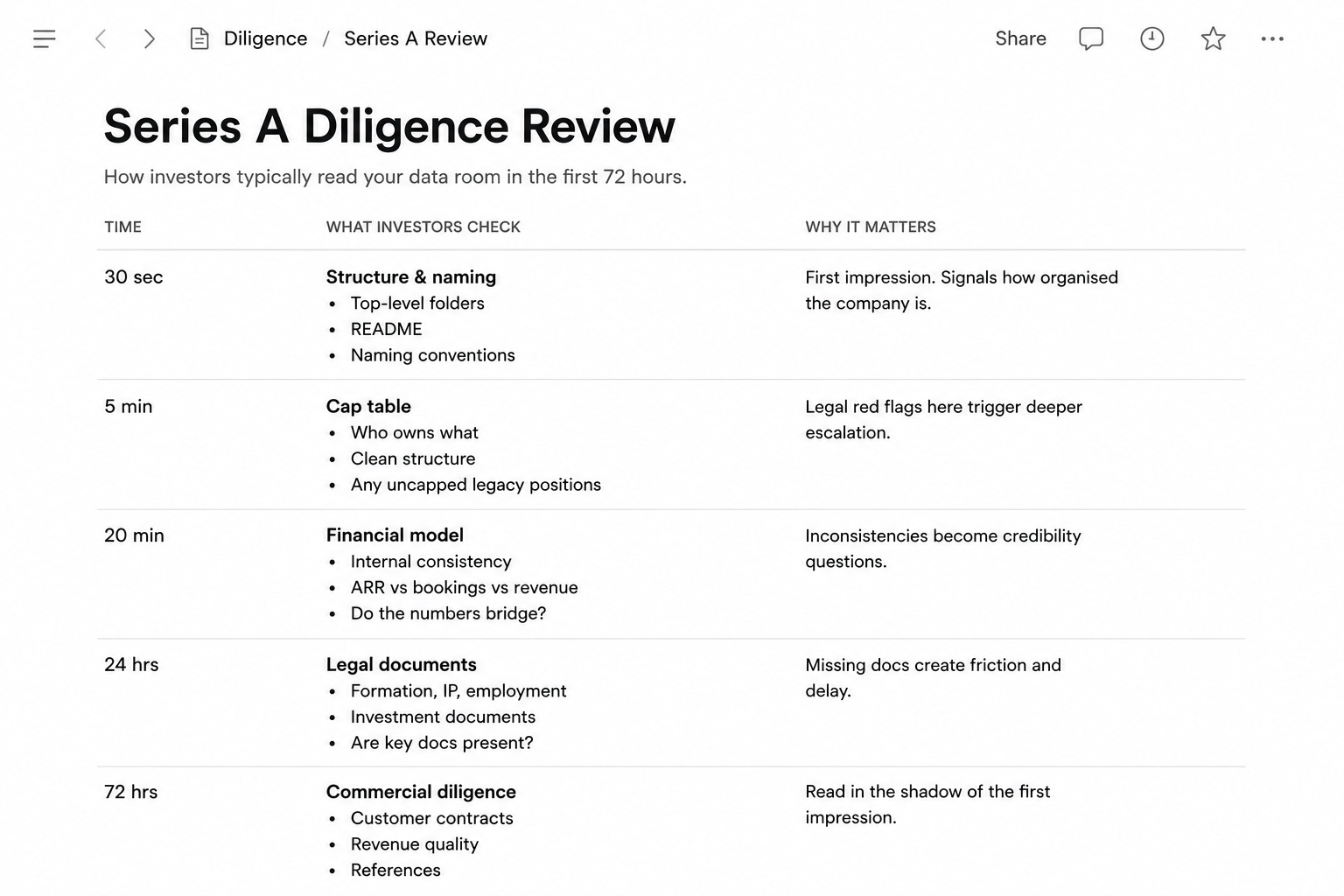

In the first thirty seconds an investor opens the top-level folder, counts the categories, checks whether there is a README, and scans the naming conventions. If the structure is chaotic, the first impression is formed immediately. That impression now colours everything that follows.

In the first five minutes they go to the cap table. Who owns what. Is it clean. Are there early contractors or investors with uncapped legacy positions. Any red flag here triggers a deeper legal escalation.

In the first twenty minutes they open the financial model. Not to check projections. To check internal consistency. ARR in the deck versus bookings in the model versus recognised revenue in the accounts. Do the numbers bridge. If they do not, this is now a credibility question, not a spreadsheet error.

In the first twenty-four hours they move to legal documents. Formation, IP assignments, employment agreements, prior investment instruments. Missing documents are flagged immediately. Every document they have to ask for adds friction and signals disorganisation.

In hours twenty-four to seventy-two they run commercial diligence. Customer contracts, revenue quality, references.

This is the critical point. All of this happens in the shadow of whatever was decided in hour one. An investor who opened a clean, well-structured room on day one reads the commercial documents looking for evidence the business is as solid as the room suggested. An investor who opened a mess reads them looking for confirmation of the concern.

You cannot fix a bad first impression in diligence. You can prevent it.

The Three Things That Kill Deals

The same failure modes appear in post-mortems of collapsed deals again and again.

Contradictory financials. ARR in the pitch deck does not equal bookings in the model does not equal recognised revenue in the accounts. These are three different measures and investors know it. When the numbers do not bridge, it is not treated as a spreadsheet error. It is treated as a signal that the founder either does not understand their own metrics or has been presenting different numbers in different contexts. This is the single most common cause of late-stage deal collapse.

Missing IP assignments. Every founder, co-founder, early employee, and contractor who created anything for the company should have signed an IP assignment agreement. Most early-stage startups have at least one gap. Legal teams are required to flag it. Even when resolved, the six-week delay it creates is often enough to lose momentum, let a competing deal close, or give an investor a reason to re-examine their conviction.

Cap table chaos. Unequal founder splits without documented rationale. Legacy investors with large, uncapped positions from early convertible notes. Missing vesting schedules. Any of these signals that governance has not been taken seriously. Which raises the question of what else has not been.

The recommended folder structure

Every VC team expects roughly the same eight categories. Deviating from this adds friction. Use this structure and number the folders so investors know the intended reading order:

📁 [Company Name] Investor Data Room

📁 01 · Pitch & Overview

└─ Current pitch deck

└─ One-page executive summary

└─ Company overview (2-pager if you have one)

📁 02 · Financials

└─ Financial model (full, with assumptions tab)

└─ P&L actuals (last 12–24 months)

└─ Cash flow statement

└─ Cap table (Carta export preferred)

└─ Bridge from ARR to bookings to recognised revenue [NOTE: this one matters]

📁 03 · Legal & Corporate

└─ Certificate of incorporation

└─ Shareholder agreement / stockholder agreement

└─ Board meeting minutes (last 12 months)

└─ IP assignment agreements (ALL founders, co-founders, contractors) ← most commonly missing

└─ Employment agreements (key hires)

└─ Prior investment instruments (SAFEs, convertibles, with full terms)

└─ Any NDAs with material parties

📁 04 · Product & Technology

└─ Product roadmap (12-month)

└─ Technical architecture overview

└─ Demo access or recorded walkthrough

└─ Any patents filed or in process

📁 05 · Commercial

└─ Key customer contracts (or anonymised versions)

└─ Pipeline data (stage, ARR, close probability)

└─ Customer reference contacts (with permission)

└─ Any signed LOIs or pilots in progress

📁 06 · Team

└─ Org chart (current + 12-month plan)

└─ Founder CVs / LinkedIn profiles

└─ Key hire plan (roles you're actively recruiting)

└─ Employment agreements (key people)

📁 07 · Market & Competition

└─ Market sizing methodology (TAM/SAM/SOM with sources)

└─ Competitive landscape analysis

└─ Third-party research supporting your market thesis

📁 08 · Board & Governance

└─ Most recent board pack

└─ Prior investor updates (last 6 months)

└─ Advisory board agreementsThe folder numbering matters. It tells the investor what order to read things in and controls the narrative arc of diligence. Start with overview, end with governance. Never bury the financials. Never put legal first (it signals you’re worried about legal).

Prompt 1: The data room audit

Before you send a single link to an investor, run this. The goal: simulate what a VC legal team will find before they find it.

Paste your complete document list (organised by folder, every file named) into Claude with this prompt. The output is a prioritised red flag list what’s missing, what naming issues will create friction, what’s likely to trigger questions, and the three highest-priority things to fix before any investor opens the room.

COPY THIS PROMPT:

You are a VC associate performing a first-pass due diligence review on a startup data room before the lead investor gives access.

Your job is to review the document list I provide and identify from an investor's perspective, not the founder's:

1. What documents are MISSING that would be expected at this stage of fundraising

2. What naming or organisation issues will create friction or signal operational immaturity

3. Which categories of legal or financial risk appear UNDERDOCUMENTED based on what's listed

4. What internal contradictions or gaps are likely to exist between the documents I've listed (e.g. cap table inconsistencies, metric definitions, prior round terms)

5. What three things I should fix or add before sending this data room to any investor ranked by investor impact, not alphabetically

Be specific to my actual list. Don't give me a generic checklist tell me what's wrong with what I have.

My context:

- Stage: [pre-seed / seed / Series A]

- Sector: [your sector]

- Prior funding: [amount raised, instruments used, e.g. two SAFEs at $5M cap and $8M cap]

- Number of founders: [X]

- Early contractors who worked on the product: [yes/no how many]

Here is my complete data room document list, organised by folder. Every file is listed by its actual name:

[PASTE YOUR FOLDER STRUCTURE AND FILE LIST HERE]

After the red flags, give me a sequencing recommendation: what should be visible immediately when an investor opens the room, what should require a second access request, and what should be held until after NDA.Run this before every round even if you think the room is ready. Founders consistently miss the same categories: IP assignment gaps (because nobody tracks who wrote what in year one), metric definition inconsistencies (because the pitch deck was written at a different time than the model), and naming conventions that seemed logical to the person who created the folders but read as disorganised to someone who’s never seen them before.

Prompt 2: The contradiction detector

This is the prompt that catches the single most common late-stage deal-killer: contradictory numbers.

ARR, bookings, and recognised revenue are three different metrics. In a well-run company at Series A, all three are tracked separately and reconciled. In most early-stage startups, the pitch deck uses the most favourable number, the model uses a different definition, and the management accounts use whichever format the accountant preferred. When an investor catches the discrepancy and they will the question becomes: which number is real, and why were different numbers used in different documents?

This prompt takes everything you give it and finds every place the numbers don’t bridge.

COPY THIS PROMPT:

I'm preparing a data room for a fundraising round and I need you to find every place where my numbers are inconsistent, use different definitions, or fail to reconcile.

I'm going to give you three things:

1. The key metrics from my pitch deck

2. The summary tab from my financial model

3. The headline numbers from my most recent management accounts

Your job is to:

1. Identify every metric that appears in more than one document and flag whether the numbers match

2. Identify every place where the same word (ARR, revenue, bookings, MRR) might be defined differently across documents

3. Tell me which reconciliation bridges are missing e.g. if ARR and recognised revenue differ, I should have a document explaining the difference

4. Flag any assumptions in the financial model that contradict the actuals in the management accounts

5. Give me, for each inconsistency, a one-sentence explanation I can put in a data room README that explains the difference to an investor before they ask

Here are my numbers:

PITCH DECK METRICS:

[Paste the key metrics slide or relevant numbers from your deck]

FINANCIAL MODEL SUMMARY:

[Paste the summary/assumptions tab from your model or the key lines: ARR, revenue, gross margin, burn, runway, growth rate]

MANAGEMENT ACCOUNTS SUMMARY:

[Paste the headline P&L numbers and any revenue breakdown]

After identifying the inconsistencies, tell me: if a VC associate reviewed these three documents in the first 20 minutes of diligence, what question would they ask first?Run this before sending the data room link. The output will almost certainly surface at least one inconsistency you hadn’t noticed not because you were being misleading, but because these documents were written at different times, for different audiences, by people who used the same words to mean slightly different things.

The first two prompts audit what you have and clean the numbers. The four prompts below build what most data rooms completely lack - and what separates the ones that close from the ones that stall.

What’s inside:

✅ Prompt 3: The narrative layer - writes the executive summaries that sit at the top of every major folder so investors read every document with context, not suspicion

✅ Prompt 4: The IP assignment audit - walks through your founding team, early hires, and contractor history and produces the complete list of who needs to sign what, in language you can actually send

✅ Prompt 5: The cap table clean-up - flags every element of your current structure that will raise investor questions and drafts the explainer notes that pre-empt them before they are asked

✅ Prompt 6: The first-72-hours sequencing guide - builds a personalised access sequence for your data room based on your stage and investor type, controlling the narrative arc of the entire diligence process

✅ The master folder template and naming convention guide - exactly how to name and structure every file, with the numbering convention that tells investors the intended reading order before they open anything

This is what a paid subscription to The Founders Corner gets you every week.

Not frameworks to screenshot and store. 50+ tools you open, use, and walk away from with something concrete, built for the decisions founders are actually making.

Prompts 3 through 6 and the folder template are available exclusively to premium subscribers of The Founders Corner.

Prompt 3: The narrative layer

Most data rooms are silent. An investor opens a folder called “Financials,” opens the model, and starts forming impressions with zero context about what they’re about to see. If the model has a note in cell A1 that says “ARR in column D is contract value, not recognised revenue see tab 3 for bridge” they’re fine. If it doesn’t and most don’t they’ll form a concern that will take two or three follow-up emails to address.

The narrative layer solves this. One short README or executive summary per folder. The investor reads it before opening anything. They know what they’re about to see, why it looks the way it does, and what the right interpretation is.

This prompt writes those summaries.