The Reason Your Round Is Taking Longer Than It Should

Most founders raise like they are hoping. The ones who close raise like they are running a process. Here is the complete six-week system

I have watched hundreds of founders raise capital. The ones who close fast share one thing that has nothing to do with their deck, their metrics, or their story.

They run a process.

Not in a manipulative way. Not in a way that feels manufactured. But they treat fundraising the way a good sales leader treats a pipeline. They know who is in play, where each conversation is, what the next step is, and when to create urgency without lying about it.

The founders who struggle are almost always doing the opposite. They are having good meetings and waiting to see what happens. They are following up when they remember to. They are treating each investor conversation as a standalone event rather than as part of a coordinated process. And they are wondering why a round that should take six weeks is stretching into six months.

The difference is not the quality of the company. It is the quality of the process.

This article gives you the operating system I have used to coach founders through more raises than I can count. The free section gives you the framework. The paid section gives you the complete six-week process with the exact tools, sequences, and Claude prompts to run it.

Why Most Fundraising Processes Fall Apart in Week Three

A fundraise has a natural momentum problem.

Week one feels good. You have meetings. Investors are taking calls. The energy is high. Week two is similar. By week three, the meetings are slowing down, some investors have gone quiet, and the founder has no systematic way to know whether the silence is disinterest or just a busy week at the fund.

By week four, the process has lost its shape. The founder is chasing some investors, ignoring others, and has no clear picture of where the round actually stands. By week six, they are extending the timeline and resetting expectations.

I have seen this happen to strong companies with good metrics and compelling founders. The round does not collapse because the company is not fundable. It collapses because the process collapses.

Three things cause it every time.

No investor pipeline discipline. Most founders track investor conversations in their head or in a loose spreadsheet. They have no systematic way to know which investors are warm, which are cooling, and which need a specific nudge to move forward. Without that visibility, they cannot manage the process. They can only react to it.

No manufactured urgency. Urgency closes rounds. Real urgency - a competing term sheet, a product milestone, a market timing argument - is the most powerful tool a founder has. But even when real urgency does not exist, a well-run process creates the perception of momentum. Investors move faster when they believe others are moving. Most founders do not engineer this deliberately. The ones who close fast always do.

No sequencing strategy. Who you talk to first matters as much as who you talk to at all. Talking to your top-choice lead investor in week one, before you have your story tight and your process running, is one of the most common and most costly mistakes founders make. The sequencing of investor conversations is a strategic decision. Most founders treat it as a calendar management problem.

The Four Metrics Every Founder Should Track During a Live Raise

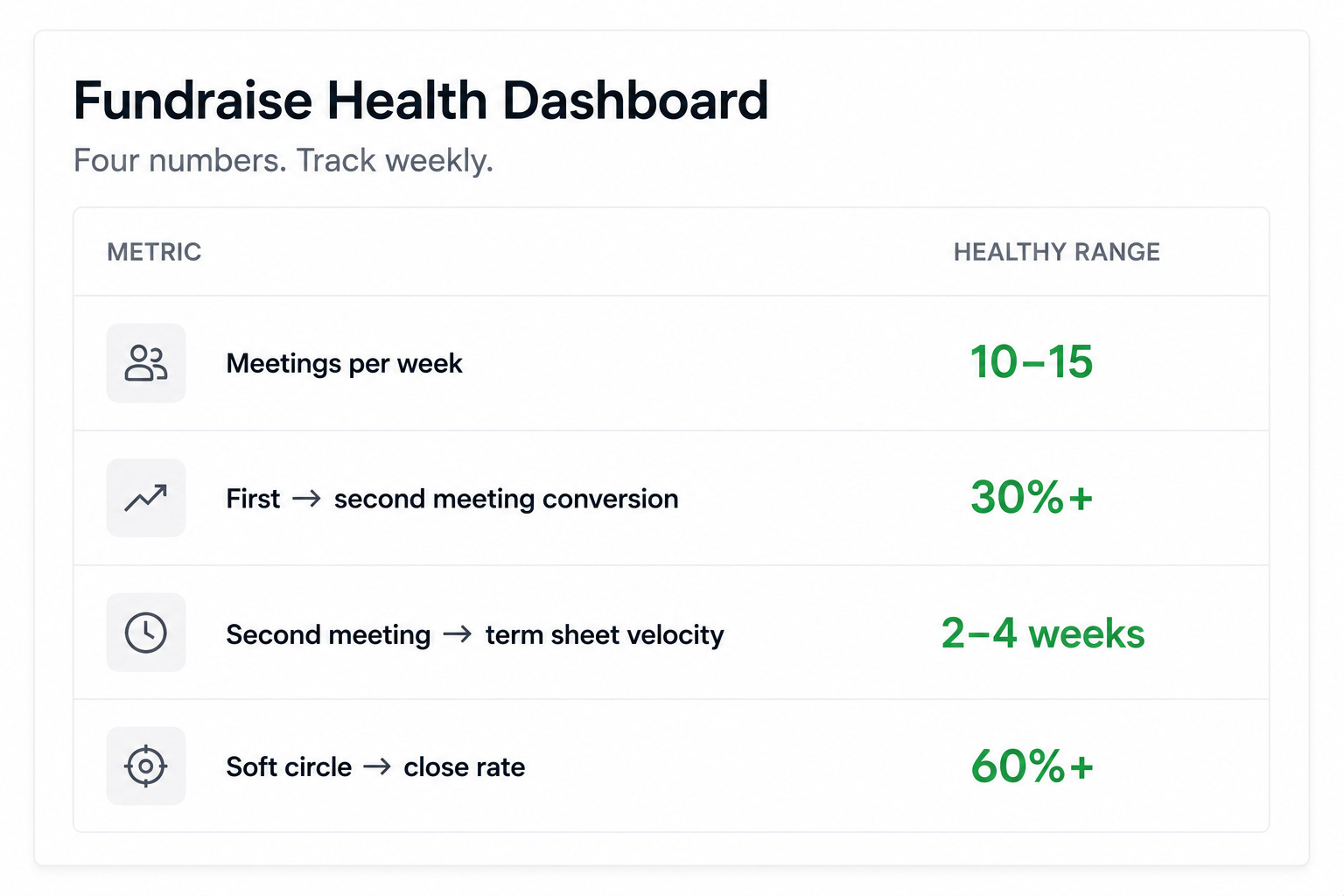

I ask every founder I work with to track four numbers throughout their fundraise. Not conversion rates. Not pipeline value. Four simple metrics that tell you whether your process is healthy or broken.

Meetings per week. A healthy seed process runs ten to fifteen first meetings in the first three weeks. If you are below that, your targeting is too narrow or your outreach is not converting. If you are above twenty, you are moving too fast and will not have time to follow up properly.

First to second meeting conversion. This is your pitch conversion rate. Industry average sits around 30 percent. If you are below 20 percent consistently, something is wrong with the pitch or the investor fit. If you are above 50 percent, you are probably not meeting enough new investors.

Second meeting to term sheet velocity. How long does it take from a strong second meeting to a term sheet? At seed, the answer should be two to four weeks. If it is stretching beyond six, the investor is not moving and you need to either create urgency or move on.

Soft circle to close rate. How many investors who express serious interest actually close? If this number is below 60 percent, you have a late-stage dropout problem - which almost always means your due diligence materials are not ready or your cap table has issues an investor discovered late.

The Sequencing Decision That Determines Everything

Before you send a single email, you need to answer one question: who do I talk to first?

Most founders answer this wrong. They go to their warm leads first, on the logic that warm conversations are easier and build confidence. This is exactly backwards.

Your warm leads are your most valuable asset in the process. Using them before your pitch is tight, before you have social proof from other conversations, and before you have any sense of urgency is like playing your best card when the stakes are lowest.

The right sequencing works like this.

In the first week, you talk to investors who are interested but not your top choice. These conversations sharpen your pitch, surface the objections you have not heard yet, and give you signal about which parts of your story land and which do not. They are practice that matters - because these investors can still write cheques - but they are not the conversations you cannot afford to lose.

In weeks two and three, you bring in your primary targets. Your pitch is tighter. You have heard the hard questions. And if any of the week-one conversations have gone well, you have the beginnings of social proof. You can say, truthfully, that other conversations are progressing.

In weeks four and five, if you have a soft circle forming, you use it to create urgency with the investors who are moving slowly. A founder who can say “we are moving toward close and I want to make sure you have the opportunity to participate” is in a fundamentally different position than one who is asking “have you had a chance to think more about this?”

The sequencing is not manipulation. It is process management. The investors who move slowly do so because they are not feeling urgency. Your job is to create it legitimately.

The Six-Week Fundraising Operating System

What follows is the complete process. Week by week. What to do, in what order, with the exact Claude prompts to run each stage.

This is not a framework. It is an operating system. The difference is that a framework tells you what to think about. An operating system tells you what to do on Monday morning.

Week One: Build the Machine Before You Turn It On

Most founders start week one by sending emails. This is wrong. Week one is infrastructure week. You are building the system before you run it.

Prompt 01: Build your investor pipeline tracker

Before you contact a single investor, you need a tracking system. Not a CRM. A simple document with five columns: investor name, fund, stage fit, contact status, and next action. Every investor you plan to contact goes in before week one ends. You should have between 40 and 80 names.

Most founders skip this step because it feels like admin. It is not admin. It is the difference between running a process and having a series of conversations. Without a pipeline tracker, you cannot know which investors are warm, which are cooling, and which need a specific nudge. You are flying blind at the moment precision matters most.

Paste your investor list into Claude with this prompt. The output is a scored, tiered pipeline you can update in real time throughout the process.

COPY THIS PROMPT:

I am preparing to raise a [seed / Series A] round of [£/$/€X].

My company is [one sentence description].

We are [pre-revenue / £X ARR / X months of growth].

Help me build a structured investor pipeline tracker.

Give me:

1. A list of the ten investor characteristics I should be filtering for at my stage

(fund size, typical check size, sector focus, geographic preference, lead vs follow appetite)

2. A scoring framework (1-3) for each characteristic so I can prioritise my list

3. The five columns every investor pipeline tracker needs and what goes in each

4. The three investor categories I should segment my list into:

Tier 1 (primary targets), Tier 2 (strong fits), Tier 3 (warm up)

5. The weekly review questions I should ask myself to keep the pipeline honestRun this before week one ends. The output becomes the document you update every day for the next six weeks. Every investor conversation, every status change, every next action goes in here. If you can see the whole pipeline at a glance, you can manage it. If you cannot, you are reacting.

Prompt 02: Write your investor outreach sequence

Cold outreach to investors has a formula. Subject line, first line, proof point, ask. Four sentences. No deck attachment on first contact. A specific ask for a 20-minute call, not a general expression of interest.

Most founders write outreach emails that are too long, too vague, and too focused on the company rather than the investor’s thesis. The investor reads dozens of these a week. The ones that convert are specific, short, and demonstrate that the founder has done enough research to know why this particular fund should care.

The mistake most founders make is writing one email and sending it to everyone. You need three versions - one for funds with a direct comparable in their portfolio, one for funds with thesis fit but no comparable, and one for warm introductions. Claude writes all three in one pass.

COPY THIS PROMPT:

I need to write cold outreach emails to investors for my [seed / Series A] raise.

Here is my company in one sentence: [description]

Here is my traction: [key metrics]

Here is why now: [timing argument]

Write me three versions of a cold outreach email, each under 100 words:

Version A: For a fund whose portfolio includes a direct comparable to my company

Version B: For a fund with no portfolio companies in my space but strong sector thesis fit

Version C: For an investor I have a weak warm connection to

(mutual LinkedIn connection, met briefly at an event)

For each version give me:

- Subject line (under 8 words)

- The email body

- The specific ask at the end

- One personalisation placeholder I should fill in for each investorWrite the three templates once. Then personalise individually for each investor and send in batches of ten to fifteen. Track open and reply rates by version. By the end of week one you will know which version is converting and can double down on the approach that works.

Week Two: Run the First Meeting and Take Notes Like a Lawyer

First meetings are not pitches. They are qualification calls. Your job is to learn as much about the investor as they learn about you. Most founders talk for 40 of the 45 minutes. The founders who close fast talk for 20 and listen for 25.

Three questions to ask every investor in a first meeting. What does the ideal version of this company look like in five years from your perspective? What would need to be true for you to move quickly on something like this? Who else in your portfolio are you most excited about right now and why?

The first two tell you whether the investor’s vision aligns with yours and what their decision criteria actually are. The third tells you what they value in a founder relationship and gives you a warm introduction opportunity into their portfolio.

If you are in market or preparing to go in market, these are the articles that will do the most work alongside this one.

→ Your Data Room Is Killing Your Round - the six prompts to fix it before you send a single link

→ The Conversation Happening About You Right Now That You Cannot Hear - what investors say in reference calls and how to get ahead of it

→ You Just Got a Term Sheet. Do Not Sign It Yet - the complete Claude prompt system for reading every clause and walking into negotiations knowing exactly where to push

The first two prompts build your pipeline and write your outreach before you send a single email. The four prompts below run the live process - and they are the difference between a round that closes in six weeks and one that drifts for six months.

What’s inside:

✅ Prompt 03: The first meeting debrief - runs immediately after every investor conversation and tells you the three signals that actually matter, the objection to prepare for, and the follow-up email to send within two hours

✅ Prompt 04: The week three re-engagement - the exact email to send when investors go quiet, written to create a reason to talk again without asking “are you still interested”

✅ Prompt 05: The soft circle conversation script - prepares you for the most important conversation in any fundraise: the direct discussion with an investor who is interested but not moving, and how to turn it into a term sheet conversation

✅ Prompt 06: The close sequence - builds your complete close plan for the final two weeks, including the deadline language that is legally defensible, the order to push investors, and the message to send everyone who did not make it into this round

This is what a paid subscription to The Founders Corner gets you every week.

Not frameworks to screenshot and store. 50+ tools you open, use, and walk away from with something concrete, built for the decisions founders are actually making.

Prompts 03 through 06 are available exclusively to premium subscribers of The Founders Corner.

Prompt 03: The first meeting debrief

Most founders finish a first investor meeting and send a generic follow-up email thanking the investor for their time. This is one of the most expensive mistakes in the process.

The follow-up email sent within two hours of a first meeting is the single highest-leverage touchpoint in the entire fundraise. It demonstrates that you listened. It shows you can execute. And it advances the conversation to a specific next step rather than leaving it open-ended. Most investors will form a preliminary view of whether they want to continue within 24 hours of the first meeting. The follow-up email either confirms or reverses that view.

Run this prompt immediately after every first meeting - ideally within an hour while the conversation is still fresh. Paste your raw notes in any format. The output is a structured debrief, a follow-up email ready to send, and an honest assessment of where this investor sits in your pipeline.