The One Fundraising Mistake Every First Time Founder Makes

Understanding the silent equity loss baked into early stage fundraising.

Founders love SAFEs.

No interest.

No maturity date.

No board drama.

Money in. Paperwork light.

It feels clean.

Until you sit down before a priced round and realise you have given away more of the company than you thought. Sometimes far more.

This article is your guide to what a SAFE really is, how it converts, and how it silently reshapes your cap table. By the end, you should be able to read any SAFE term sheet and understand exactly what you are committing to, and how your ownership shifts the moment real equity appears.

I have been building out a growing library of tools to help founders navigate these decisions with precision rather than instinct. New tools are released that map directly to the topics I write about. Today’s article leads into the latest addition to that library, a SAFE Dilution Calculator designed to show you the real effect your SAFEs have on your future ownership.

Table of Contents

1. What A SAFE Actually Is

2. The Core SAFE Levers

3. Dilution Fundamentals You Must Know Cold

4. How SAFEs Convert In A Priced Round

5. Why SAFEs Create Surprise Dilution

6. Using SAFEs Intelligently

7. How Investors Analyse Your SAFEs

8. Bringing It All Together

9. See What This Looks Like For Your Company

1. What A SAFE Actually Is

A SAFE is a Simple Agreement for Future Equity.

It is not debt, there is nothing to repay.

It is not equity today, there are no shares, no vote, no board presence.

It is a contract that says:

“You give me money now. I get equity later, when a specific fundraising event happens.”

That event is almost always your next priced round.

Until that moment, the SAFE holder sits in a kind of economic shadow. They do not appear on the cap table, but the claim they hold against your future equity is very real.

This is the foundation of SAFE driven dilution. The ownership does not show up until the conversion event. When it does, it lands all at once.

2. The Core SAFE Levers

Everything about dilution comes down to four ideas.

Valuation cap.

Discount.

Whether the SAFE is pre money or post money.

Pro rata rights.

2.1 Valuation Cap

The valuation cap is the maximum company valuation at which the SAFE converts. If your next round is priced above the cap, the SAFE converts at the cap instead.

Imagine you raise at a $20,000,000 pre money valuation, but earlier you issued a SAFE with an $8,000,000 cap. That investor now converts at $8,000,000, not $20,000,000. They receive more shares than the new investor for the same dollar invested. A lot more.

2.2 Discount

A discount allows a SAFE investor to convert at a percentage below the next round price.

10%.

15%.

20%.

If the next round price per share is $1.00 and the SAFE has a 20% discount, that SAFE converts at $0.80 per share.

Many SAFEs allow the investor to choose whichever is more favourable, the cap or the discount.

2.3 Pre Money versus Post Money SAFEs

Pre money SAFEs often leave founders unable to calculate true dilution until conversion.

Post money SAFEs allow exact ownership to be calculated immediately.

For example, a $250,000 SAFE on a $6,000,000 post money valuation gives the investor 4.17% ownership.

Post money SAFEs remove ambiguity, and they remove optimism.

2.4 The ASA for UK founders

For founders in the United Kingdom, there is also the ASA, known as an Advanced Subscription Agreement. It plays a similar role to a SAFE but is structured to comply with SEIS and EIS rules, which makes it far more relevant for UK angels and early stage investors.

The biggest functional difference is timing. An ASA typically must convert into shares within six months to remain compliant. If that conversion does not happen via a priced round within that period, the ASA usually converts at the valuation cap set out in the agreement, regardless of what the next round looks like.

The mechanics feel similar to a SAFE, but the time pressure and SEIS or EIS constraints mean founders need to be more disciplined in how and when they use ASAs.

3. Dilution Fundamentals You Must Know Cold

Pre money is the value of the company before the new round.

Post money is pre money plus the money raised.

Investors calculate ownership as:

investment ÷ post money valuation

Option pools complicate this because investors usually require the pool to be increased before their investment is counted, pushing that dilution onto founders and SAFE holders.

4. How SAFEs Convert In A Priced Round

You negotiate the valuation.

You agree the option pool.

You calculate the new investor’s shares.

Then all SAFEs convert.

A simple SAFE stack

You own 10,000,000 shares.

There is no option pool yet.

You have three post money SAFEs:

$250,000 at a $6,000,000 cap

$500,000 at an $8,000,000 cap

$250,000 at a $10,000,000 cap

You now raise $3,000,000 at a $12,000,000 pre money valuation.

Step 1: Compute SAFE ownership

$250,000 on $6,000,000 → 4.17%

$500,000 on $8,000,000 → 6.25%

$250,000 on $10,000,000 → 2.50%

Total SAFE ownership → 12.92%

Step 2: Add the new investor

A $3,000,000 investment on a $12,000,000 pre money valuation results in a $15,000,000 post money valuation.

This implies 20% ownership for the new investor.

Approximate post round structure:

Founders → 67.08%

SAFE holders → 12.92%

New investor → 20%

Before the option pool.

Add a 10% pool and founder ownership falls further.

5. Why SAFEs Create Surprise Dilution

5.1 Dilution is invisible until it is not

Your cap table does not change when you sign a SAFE.

It feels like the dilution is not real.

Then everything converts at once.

5.2 Multiple caps compound

A pre seed SAFE.

A seed extension.

A strategic angel cheque.

Individually small.

Together often 10% to 20%.

5.3 Pre money SAFE mechanics

Pre money SAFEs dilute founders more than expected because later SAFEs dilute earlier ones indirectly.

5.4 Option pools hit you before investors

Investors require the option pool to be increased before their investment.

The dilution falls on founders and SAFE holders, not the new investor.

6. Using SAFEs Intelligently

Think in ownership, not cash

Ask:

“How much dilution can I absorb before my priced round?”

Track your post money exposure

Record for each SAFE:

Amount

Cap

Implied %

Total it.

If it crosses your comfort threshold, stop issuing SAFEs.

Harmonise terms

Consistent caps and terms prevent unpredictable conversion outcomes.

Model ahead

Before signing a SAFE, model:

Expected pre money valuation

Planned raise amount

Required option pool

Then measure founder ownership.

7. How Investors Analyse Your SAFEs

Investors reverse engineer your cap table.

If they see:

High early dilution

Low founder ownership

Inability to hire senior talent

They worry.

Sometimes they walk away.

8. Bringing It All Together

A SAFE is quiet when signed and loud when it converts.

If you understand caps, discounts, pre money structures, post money structures, and option pools, you can use SAFEs strategically.

If you do not, they quietly compound and erode ownership.

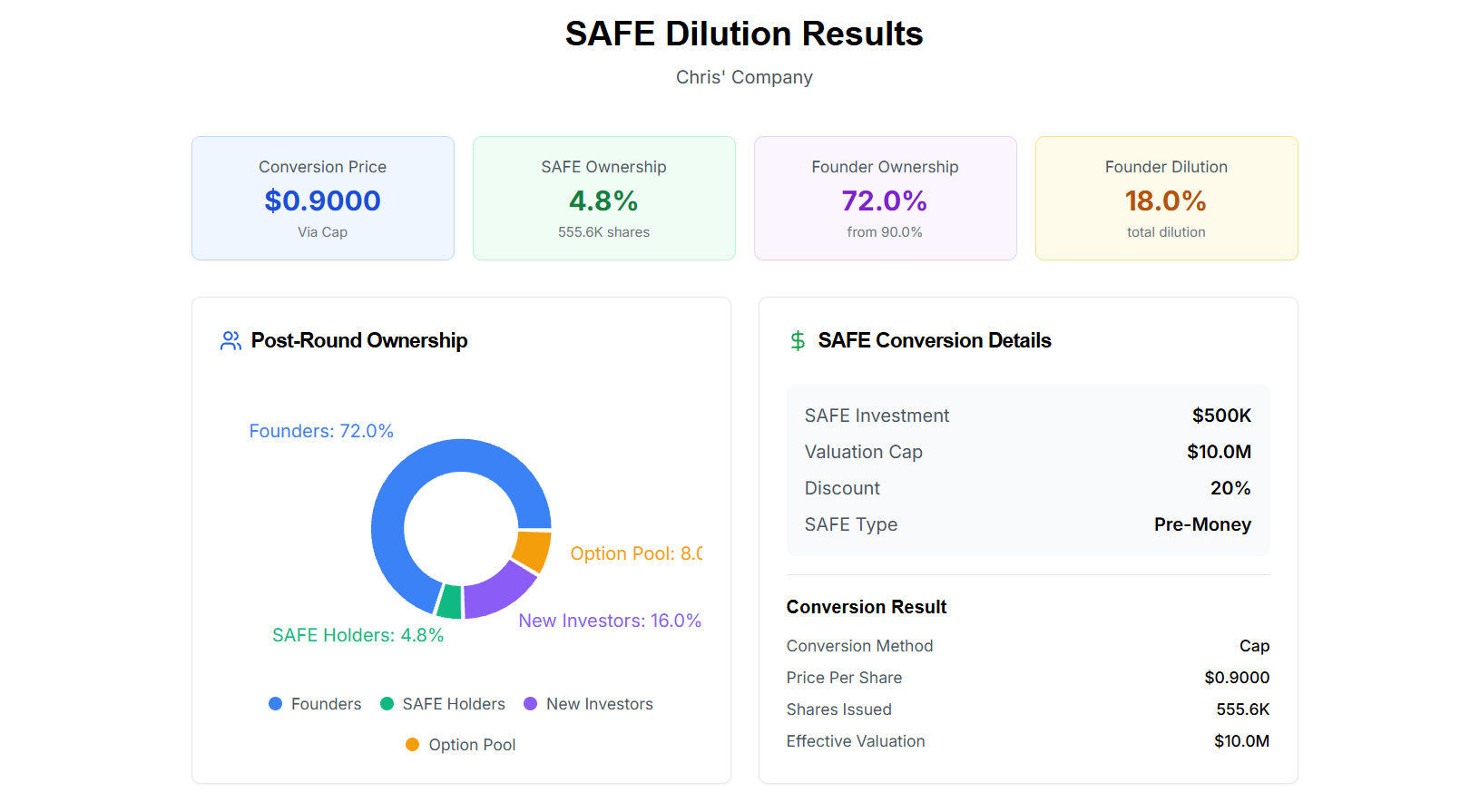

9. See What This Looks Like For Your Company

The theory matters.

But seeing real numbers is decisive

The SAFE Dilution Calculator lets you:

Enter every SAFE

Capture caps, discounts, and SAFE types

Model different future valuations and raise sizes

See exact founder, investor, and pool ownership across scenarios

If you want clarity before your next raise:

Get access to the SAFE Dilution Calculator below.

Keep reading with a 7-day free trial

Subscribe to The Founders Corner® to keep reading this post and get 7 days of free access to the full post archives.