The Conversation Happening About You Right Now That You Cannot Hear

Most founders spend months preparing for the partner meeting. Nobody prepares for what comes after it.

The partner meeting went well. You felt it in the room. The questions were hard but you handled them. The champion walked you out and said they would be in touch soon.

Three days later, an email arrives.

“We’re in the process of speaking with a few of your references. Could you send over contact details for two or three people who know your work well?”

You send the names. You go back to running the company.

And then a conversation starts that you are not on, cannot hear, and cannot correct in real time.

For most founders, the reference call is the most consequential thirty minutes of the entire fundraise. It is also the thirty minutes they have prepared for least.

What the Reference Call Actually Is

Most founders think of the reference call as a formality. A box-ticking exercise. Something that happens after the decision has effectively been made.

It is not.

The reference call is the last piece of information an investor collects before deciding whether to issue a term sheet. By this point they believe in the business. They believe in the market. The question they are still answering is whether they believe in you.

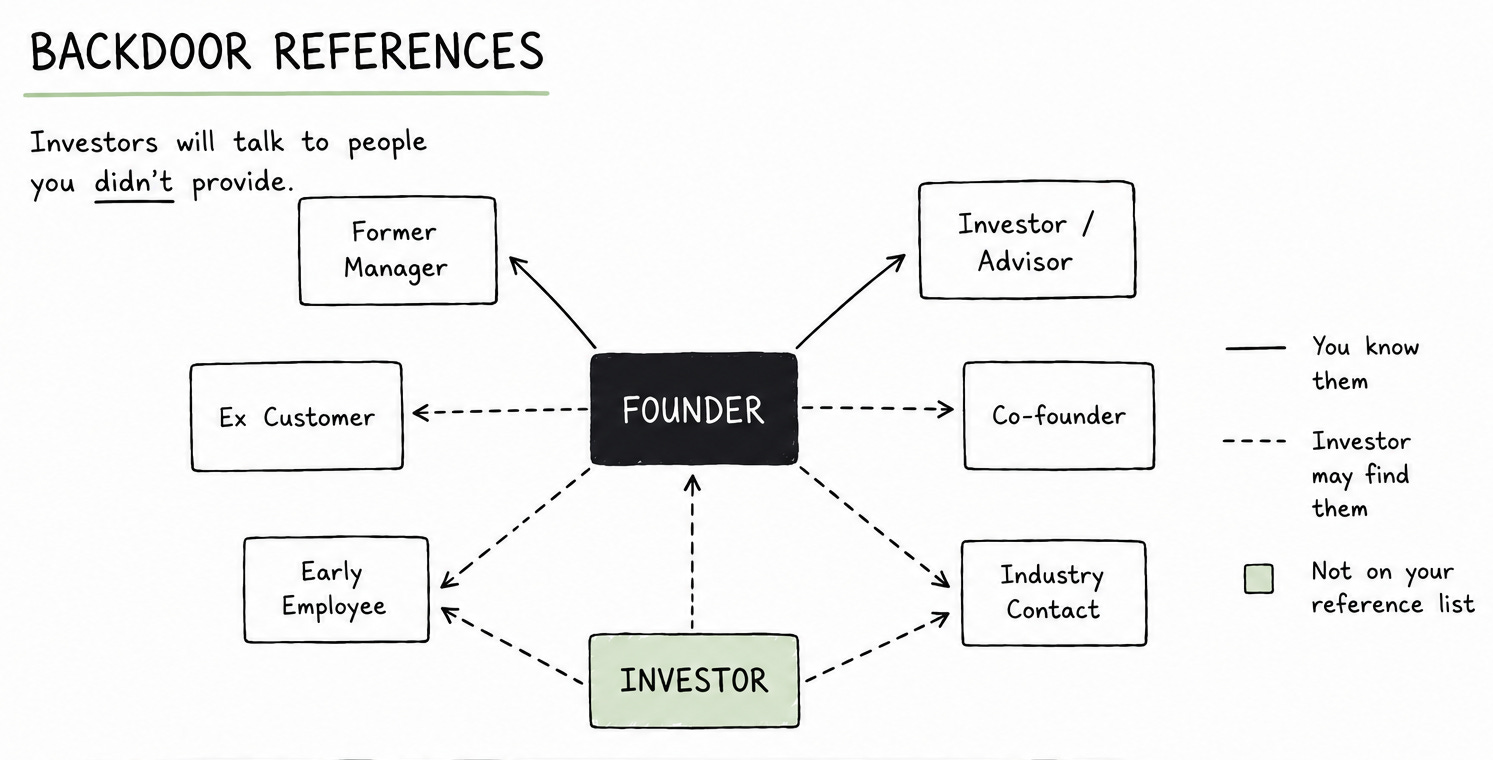

And they are answering it by talking to people who have worked with you, been led by you, been a customer of yours, or watched you operate up close. People you chose. And in some cases, people you did not.

Investors run backdoor references. They find people in your network through their own connections, through LinkedIn, through the portfolios of your existing investors. They call people you did not provide and ask the same questions. Sometimes they call people you specifically hoped they would not.

Most founders have no idea this is happening.

What Investors Are Actually Asking

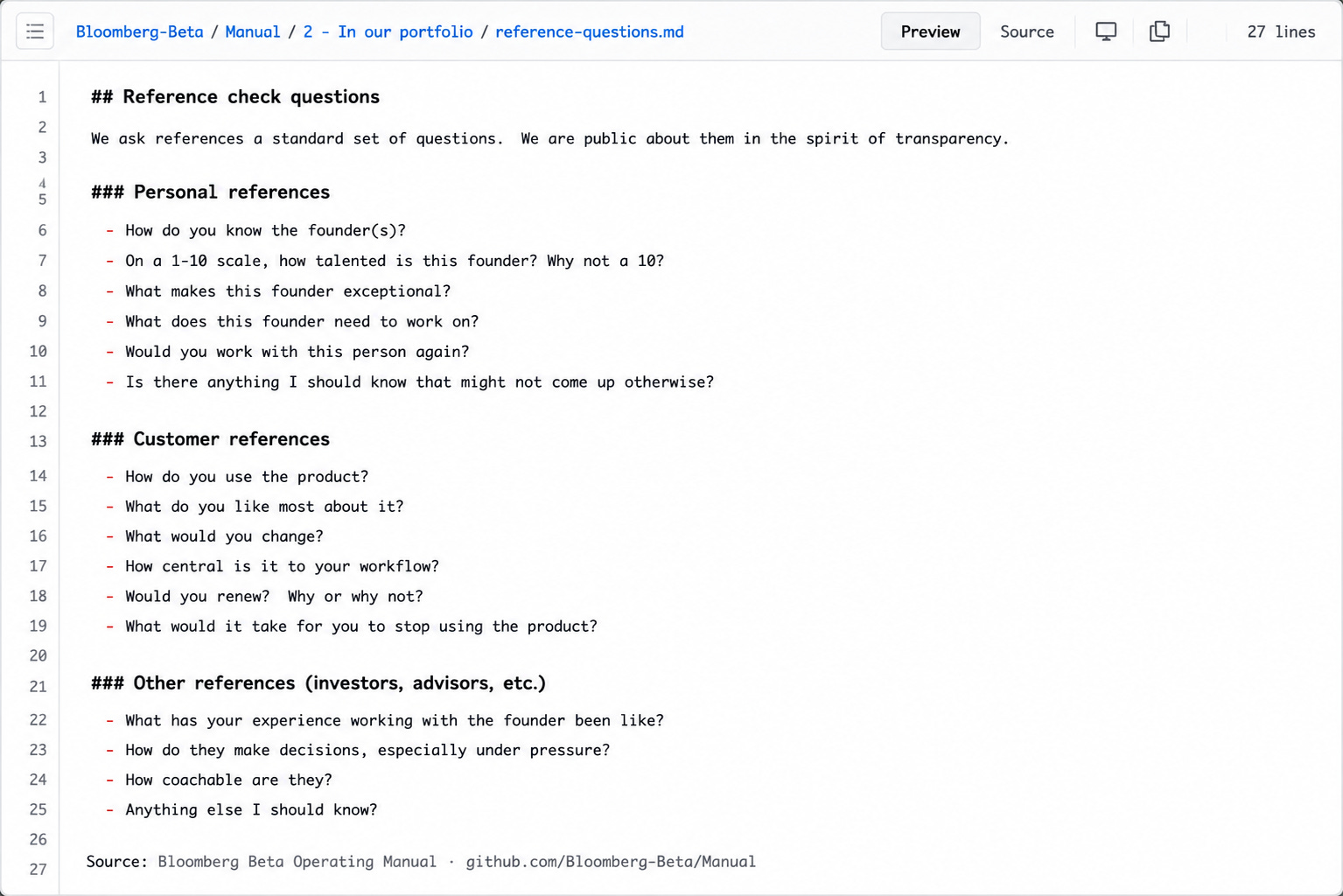

The questions investors ask in reference calls are not the questions founders expect.

They are not asking whether this is a good business. They have already formed a view on that. They are asking five things.

Whether the story you told in the partner meeting is true. Whether you can lead a company, not just build a product. Whether there are patterns of behaviour in your past that contradict what you presented. Whether you are self-aware and coachable. And whether your customers are actually customers - paying, renewing, and central to their operations.

The question that catches most references off guard is this one: “What does this founder need to work on?”

Every investor asks it. Most references are not prepared for it. And the way they answer it tells an investor more about you than almost anything else on the call.

A reference who says “nothing comes to mind” is not credible. Investors know everyone has something to work on. A reference who says something vague like “she can be a bit intense sometimes” opens a question the investor will now spend the next three conversations trying to answer.

A reference who says “she has been working on giving feedback earlier rather than letting things sit. I have seen her get noticeably better at it over the last eighteen months” is the answer investors are hoping for.

The difference between those two answers is not the truth. It is preparation.

The Reference Most Founders Do Not Think About

There are two types of references in every fundraise. The ones you provide. And the ones investors find themselves.

The ones you provide you can prepare. The ones they find themselves you cannot.

Which means the most important reference preparation you can do is to know your own network before diligence starts. If there is someone in your past, a co-founder who left, an early employee who departed unhappily, a customer relationship that ended badly, know who they are before an investor calls them.

You cannot control what they say. But you can get ahead of it. If there is a difficult chapter in your history, surface it with your investor before diligence begins. Self-disclosure builds more trust than discovery.

Who to Use as a Reference and Who Not To

Not everyone who likes you is a good reference. The person who thinks you are extraordinary needs to be able to say why, with specifics.

The strongest references for a Series A fundraise are former managers or employers who saw you perform under pressure. Early customers who are paying, renewing, and can describe the commercial terms. Co-founders or early team members who can speak to how you make decisions under adversity. And investors or advisors who have seen enough founders to contextualise you against others at your stage.

The references that hurt your raise are the ones who speak in generalities. “She’s incredibly smart and really driven” is not a strong reference for a CEO. It is the reference you give when you cannot say more than that. Investors hear the absence of specifics as the presence of doubt.

Customer references deserve special attention. Investors call your customers to verify, not to be reassured. They ask whether the customer is actually paying, what they pay, whether they would renew, and how central the product is to their business. A pilot customer or a friendly logo who has not yet paid is not a reference. It is a liability.

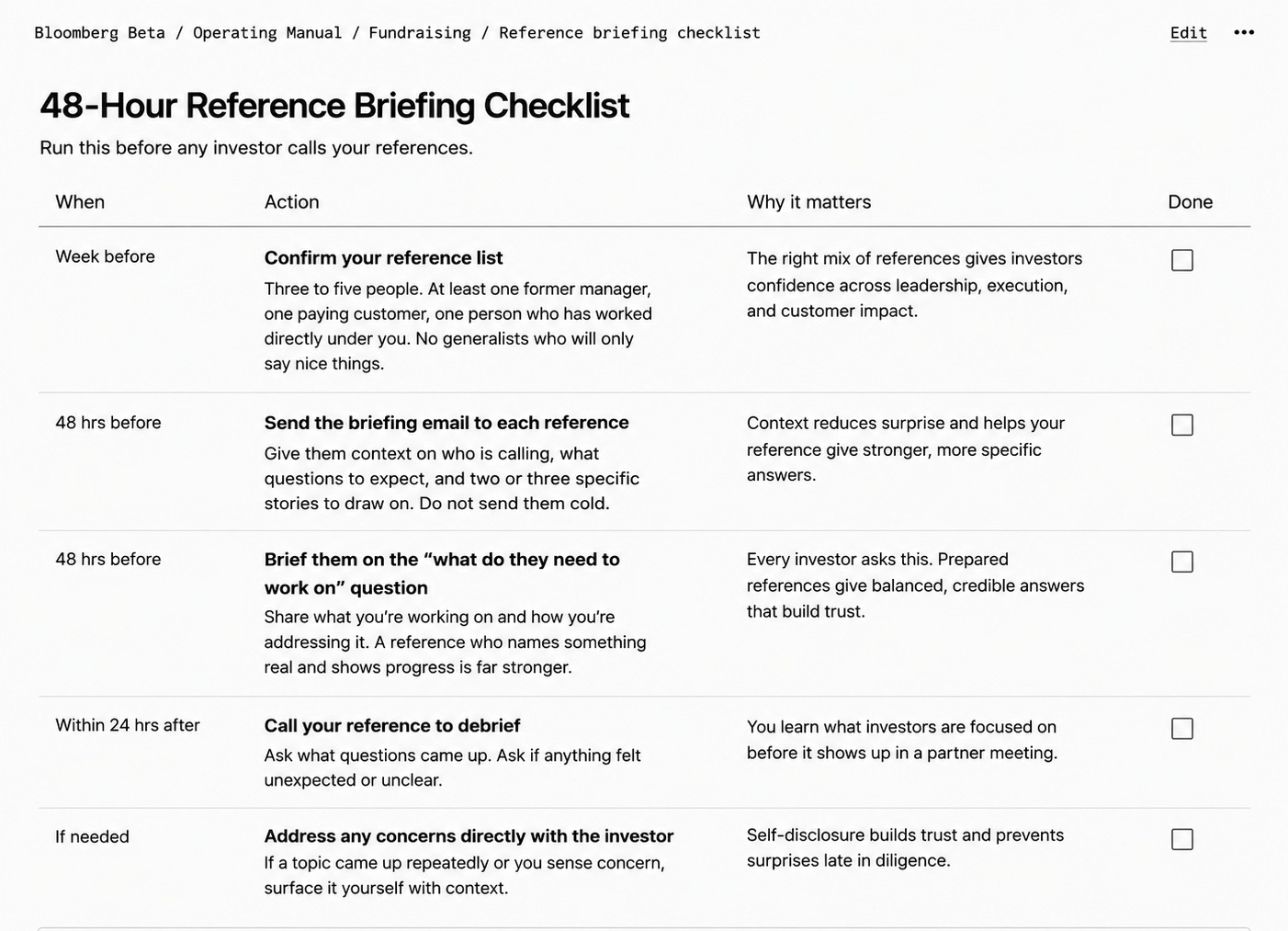

How to Brief Your References Before the Call

Send a short email to each reference at least 48 hours before an investor calls them. The Reference Check Playbook below includes the full briefing template. Here is what it needs to do.

First, give them context on who is calling and why. References who go into the call cold spend the first five minutes figuring out what is happening. That is five minutes not spent talking about you.

Second, tell them what questions to expect. Not so they can rehearse answers. So they are not caught off guard by questions like “what does this founder need to work on?” A reference who has thought about that question in advance gives a much better answer than one who is thinking about it for the first time with an investor on the other end of the line.

Third, give them two or three specific stories to draw on. Not talking points. Stories. Specific moments that illustrate something real about how you operate. The quarter the company nearly ran out of money and what you did. The team conflict you navigated and how. The customer you lost and what you changed because of it.

Investors trust references who tell specific stories more than references who give general praise. You are not telling your references what to say. You are giving them the raw material to say it well.

What to Do After the References Are Called

Most founders do nothing after their references are called. That is a mistake.

Call your references within 24 hours of the investor call. Ask what questions came up. Ask whether anything felt unexpected. Ask if the investor probed on anything that surprised them.

This is how you find out what investors are focusing on in the final stages of diligence. And whether there is something you need to address directly.

If a reference flags that a specific question came up repeatedly, or that the investor seemed to dwell on a particular topic, address it with your investor directly. Do not wait for them to raise it.

“I heard from one of my references that the question of team concentration came up. I wanted to give you more context on that directly” is a much stronger move than hoping they will not mention it in the next partner meeting.

Thank your references regardless of the outcome. A short personal note after the process closes, whether the deal happens or not. References are a relationship, not a transaction. The founders who build the best investor networks treat them accordingly.

The Frame to Take With You

Most founders treat the reference check as something that happens to them. The best founders treat it as something they design.

You cannot control what your references say. But you can control who you ask, what context they have before the call, and what stories they are prepared to tell. That is not manipulation. That is preparation.

The deal you have spent six months building can turn on a twenty-minute phone call you are not on. A phone call where the questions are predictable, the answers are shapeable, and the outcome matters more than almost anything else in the final stages of diligence.

Most founders leave this entirely to chance.

If you are preparing for a fundraise in the next 90 days, these are the issues that will do the most work alongside this one.

→ The Data Room That Doesn’t Lose Deals - the 48-item checklist investors work through before they call your references, and the five documents that kill the most deals at the last minute

→ You Got the Partner Meeting. Now What? - how to read the room before the investment decision is made, and how to follow up in the 24 hours after

→ The Call Your Investor Wants You to Take Unprepared - what happens when your existing investor offers to lead your next round, and the five terms to negotiate before you say yes

The Reference Check Playbook

The Reference Check Playbook is a five-section working document built from the exact process I use when preparing portfolio founders for investor due diligence.

It is not a summary. It is not a checklist you glance at once and close. It is the document you open the moment an investor asks for references, and return to after every call.

What’s inside:

✅ How to Choose Your References - who to use, who to avoid, and how to think about the references investors find themselves without telling you

✅ The Reference Preparation Sheet - complete one for each reference before you provide their details. Feeds directly into the briefing template.

✅ The Reference Briefing Template - the complete email to send to each reference at least 48 hours before an investor calls them, with guidance on exactly what stories to brief them on

✅ The Reference Scorecard - fill in one per reference after the investor calls them. Tracks every question asked, which topics the investor dwelled on, and what you need to address before the next partner meeting

✅ After All References Are Called - how to use the scorecards together to spot patterns and close down concerns before they become deal blockers

This is what a paid subscription to The Founders Corner gets you every week.

Not frameworks to screenshot and store. 50+ tools you open, use, and walk away from with something concrete, built for the decisions founders are actually making.

The Playbook is available exclusively to premium subscribers of The Founders Corner.