The Claude Prompt That Found My Real ARR. Then I Raised.

The controversy is real. So is the fix. Nine Claude prompts that find your true ARR, and the words to defend it

There’s something nobody tells you about pitching right now, until an investor asks you to prove it:

The number on your slide isn’t your ARR anymore. It’s a claim about your ARR, and this year, investors are trained to make you back it up.

If you built your deck the way founders have built decks for a decade (take your best month, multiply by twelve, call it ARR) you’ve been preparing for a question nobody used to ask out loud. They ask it now. Often in the first meeting, sometimes before your deck is even open.

The founders getting through diligence cleanly this year aren’t necessarily the ones with the biggest number. They’re the ones who already know, before anyone asks, exactly which part of that number is real.

Why every investor just started asking this question 📊

In April, Scott Stevenson (founder of the legal AI startup Spellbook) said publicly what most of the industry had only said quietly in board meetings: many AI startups are “crushing revenue records” using a metric that doesn’t mean what it says. TechCrunch picked it up. Chamath weighed in. Garry Tan posted his own breakdown of what “correct” revenue reporting looks like. By the end of the month, the debate had a name: the ARR trap.

Here’s the mechanic underneath it. ARR is not a GAAP metric. No accounting standard defines it. No auditor certifies it. No regulator checks it. It can mean whatever the founder needs it to mean in the room. A month of recurring revenue, multiplied by twelve, gets presented the same way whether it’s collected, contracted but not yet billed, or a free pilot the sales team is hoping converts.

Most advice after the controversy stopped at “be more honest about your number.” True. Not enough.

The founders coming out ahead of this aren’t relabelling a slide. They’re using the real number to answer three questions most people skip: is the business as strong as they thought, has their fundraise timeline moved, and what do they say when an investor asks the obvious follow-up.

That’s what this system does. Not one prompt that hands you an uncomfortable number and leaves you with it. Nine, in the order you actually need them.

The three words doing all the damage: ARR, CARR, and “revenue”

More rounds are getting stuck here than founders realise, and usually not because the revenue isn’t real.

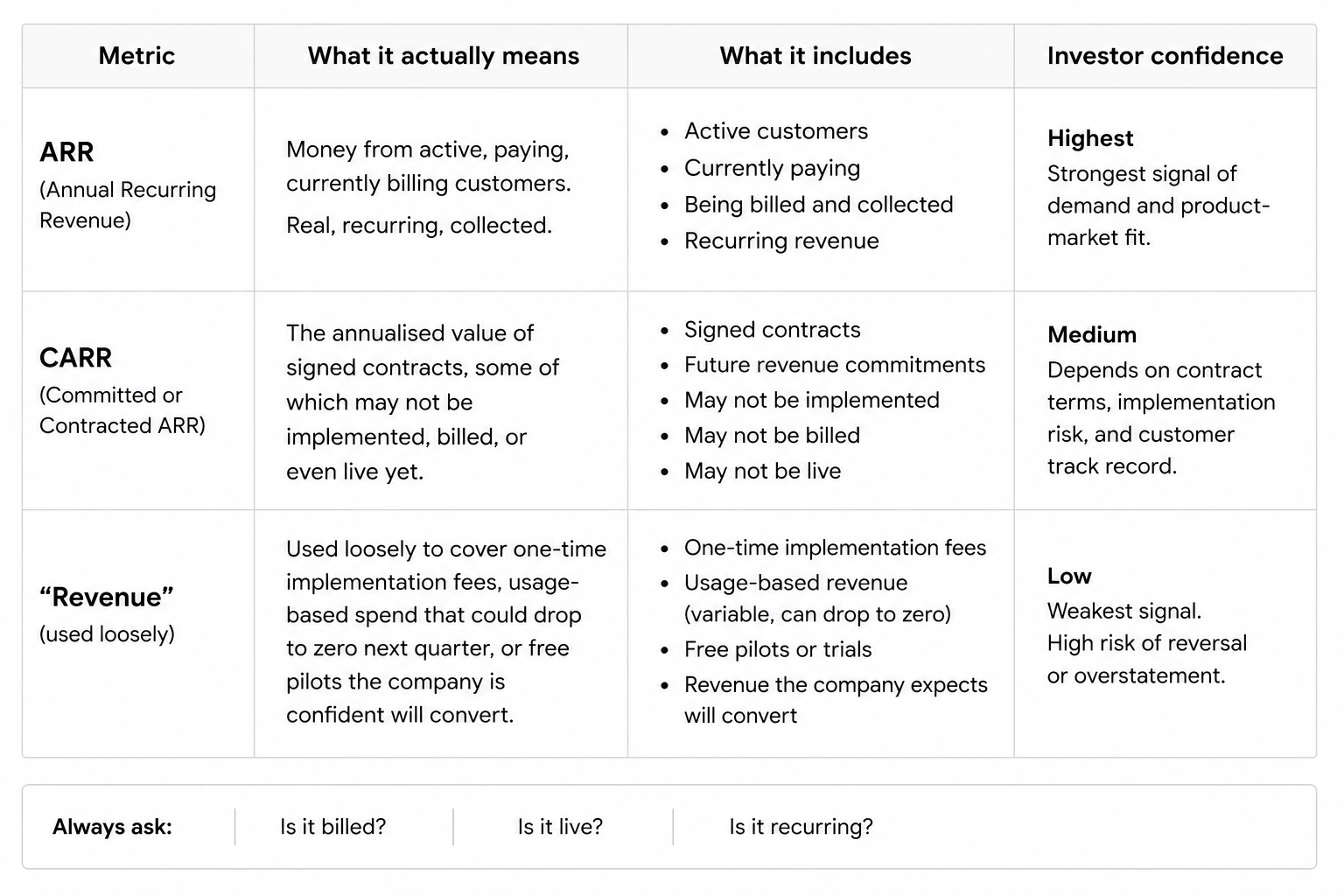

ARR (Annual Recurring Revenue): money from active, paying, currently billing customers. Real, recurring, collected.

CARR (Committed or Contracted ARR): the annualised value of signed contracts, some of which may not be implemented, billed, or even live yet.

“Revenue” used loosely to cover one-time implementation fees, usage-based spend that could drop to zero next quarter, or free pilots the company is confident will convert.

None of these are illegitimate numbers to have. The problem isn’t that CARR exists. It’s that CARR gets reported as ARR, with no footnote distinguishing the two. That gap surfaces the moment a diligence team pulls the contract register.

Some late-stage rounds are being priced against ARR figures that overstate the real base by half or more, according to analysis after the controversy. One widely cited Series A benchmark found companies with 120%+ net revenue retention commanding roughly 2.5x higher valuations than companies hitting the identical ARR number with 90% retention. The market is already pricing quality over quantity. Most founders haven’t caught up to that yet.

The run-rate method itself isn’t the issue. One month of revenue times twelve is standard practice, even among the largest AI labs, according to Bloomberg’s reporting on the controversy. What critics flagged was CARR, pilot revenue, and non-recurring fees folded in without being labelled. Diligence teams are now explicitly scoped to request contracted-versus-recognised revenue waterfalls. That document barely existed as a standard ask two years ago.

The founders this hits hardest are the honest ones who’ve never separated their own number. If you’ve never split your reported ARR into “collected,” “contracted but not billed,” and “everything else,” you don’t know which founder you look like when someone asks.

Do you actually know your real number? Five questions to find out

1. Can you state your ARR without the word “roughly”? If your honest answer starts with “it’s roughly” or “call it about,” you’re quoting a headline figure, not a number you’ve actually reconciled against your contract register.

2. What percentage of your ARR is billing today, versus signed but not yet implemented? Most founders have never calculated this split. Every serious diligence process will.

3. Does any single customer represent more than 15% of your total ARR? If you had to answer that question out loud right now, would you know it, or would you need to go and check?

4. Is your net revenue retention trending up or down over the last two quarters? Not where it sits today. Where it’s heading. A flat 100% moving toward 90% tells an investor something a single snapshot never will.

5. If your biggest customer churned tomorrow, could you say exactly what that does to your real ARR, without opening a spreadsheet? If the honest answer is no, you don’t currently have command of your own number. This system exists to fix that before someone else finds the gap first.

🟦 Prompt 1: The ARR reclassification audit

Do this one first, alone, before you show it to anyone, including your co-founder. You’ll need your actual contract or customer list, not your dashboard’s headline number. If you don’t have that broken out anywhere, that’s the first finding.

I'm going to give you a list of my company's customers or contracts,

with the value and status of each. Reclassify my total reported ARR

into the categories a sophisticated investor's diligence team would

use, not the category my dashboard currently reports it in.

For each customer or contract, sort into exactly one bucket:

1. COLLECTED ARR: actively billing, payment received in the last

billing cycle, no signs of imminent churn

2. CONTRACTED, NOT BILLED (CARR): signed contract, annualised value

is real, but implementation hasn't started or first invoice hasn't

gone out yet

3. USAGE-BASED OR VARIABLE: revenue that depends on ongoing usage and

could shrink without a contract violation (real revenue, but should

never be annualised as if it's fixed)

4. PILOT, TRIAL, OR NON-PAYING: anything free, discounted below normal

pricing as a trial, or not yet a committed paying relationship

5. ONE-TIME OR NON-RECURRING: implementation fees, one-off services,

anything that isn't going to repeat next year

Give me:

- The total for each bucket

- My "headline" ARR as I've been reporting it, next to my true

Collected ARR

- The percentage gap between the two numbers

- A one-line flag for anything in my current external materials

(deck, website, one-pager) that states the headline number without

qualification

Here's my customer or contract data:

[PASTE CUSTOMER LIST WITH VALUES AND STATUS]💡 Why this works: Almost every founder who runs this for the first time is surprised by the gap, not because they were lying, but because ARR dashboards default to counting signed contracts the moment they’re signed, whether or not implementation has started. The gap between your headline number and your Collected ARR is exactly what a diligence team is now trained to go looking for.

If this is useful, don’t stop here.

This same pattern (raw numbers in, a real answer out) runs through everything we build here. A few more worth your time:

The Claude Guide Every Founder Should Run Before Fundraising: the nine prompts that replicate how modern VC firms screen your deck with AI before a partner ever opens it

The Claude Prompt That Turns a Cold Email Into One a VC Actually Reads: the five-prompt system behind the outreach that gets a reply instead of an archive

The Two-Minute Investor Briefing Every Founder Should Be Running: a Claude research agent that builds a full investor briefing before every meeting

I Asked Claude to Reject My Pitch Until It Couldn’t. Then I Raised.: the adversarial prep system that finds every weak point in your pitch before an investor does

How to Build Your Fundraising Narrative With Claude: the five-prompt playbook for turning your raw story into the argument that actually closes rounds

🟦 Prompt 2: The retention and concentration check

The controversy shifted the conversation from “how big is your ARR” to “how good is it.” Two numbers now do more work in an investor’s head than the top-line figure: net revenue retention, and how concentrated your revenue is in a small number of accounts.

Using the same customer or contract data from before, calculate:

1. NET REVENUE RETENTION: expansion revenue plus retained revenue,

minus churned and contracted revenue, as a percentage of revenue

from the same cohort a year ago. If I don't have a year of data,

tell me what proxy calculation to use instead and its limitations.

2. LOGO CONCENTRATION: what percentage of my total ARR sits in my

top 3 customers? Top 5? Flag if any single customer represents

more than 15% of total ARR, a common diligence red-flag threshold.

3. COHORT TREND: if I have month-by-month history, tell me whether my

retention is trending up or down over the last two quarters, not

just where it sits today.

4. THE HONEST HEADLINE: write me the single sentence I should be

saying out loud about my revenue quality, one that would hold up

if an investor asked a sceptical follow-up question immediately

after.

Here's my additional data: [PASTE MONTH-BY-MONTH HISTORY IF AVAILABLE,

OR TELL CLAUDE WHAT YOU DON'T HAVE YET]💡 A $2M ARR number with 130% net revenue retention and no customer over 10% of the book is a stronger fundraising story than a $4M ARR number concentrated in two logos with 85% retention, even though it’s half the size. Most founders have never seen these two numbers side by side for their own company. Investors now build them by default.

🔒 You’ve found your real number. Here’s what turns it into the one an investor actually signs off on.

Everything above already puts you ahead of most founders walking into their next raise. Here’s exactly what’s waiting below the paywall:

✅ Prompt 3: The margin reality check. What you’re actually keeping per customer once compute and inference costs are counted, not what your top-line ARR implies.

✅ Prompt 4: The contract conversion plan. Turns your signed-but-not-billed CARR into real, collected revenue, customer by customer, before your next board meeting.

✅ Prompt 5: The runway recalculation. Reruns your burn multiple and months of runway against your true Collected ARR, and tells you plainly whether your fundraise timeline just moved.

✅ Prompt 6: The sceptical investor simulation. Claude plays the partner who’s read the ARR controversy and asks the exact follow-up questions your materials don’t yet answer.

✅ Prompt 7: The transparent disclosure rewrite. The specific language for presenting a real, labelled number that reads as command of the business, not a confession.

✅ Prompt 8: The board-versus-investor reconciliation. Makes sure your board deck and your investor deck are telling the same story, in the same words.

✅ Prompt 9: The category contrast play. Turns your own transparency into a quiet differentiation point against competitors still quoting the inflated number.

✅ The full nine-prompt sequence, copy-paste ready, built to adapt to your own company’s revenue model. Swap in your categories, your customer names, and your thresholds, and run it before every board meeting and every investor conversation.

Paid subscribers also get:

✅ 60+ additional tools covering every other stage of fundraising and running a company: pitch deck screening, investor research and outreach, meeting prep, term sheet analysis, and data room management. The same tool stack this ARR workflow came from.

🟦 Prompt 3: The margin reality check

This is the number the ARR controversy mostly skipped over. It decides whether the business underneath the revenue actually works.

Keep reading with a 7-day free trial

Subscribe to The Founders Corner® to keep reading this post and get 7 days of free access to the full post archives.