The Claude Due Diligence Playbook That Gets You to Closing

Diligence isn’t a formality. It’s where the deal actually gets decided.

Founders treat the term sheet like the finish line.

It isn’t.

15% to 25% of signed term sheets never make it to a closed round.

Not because the business got worse. Because diligence found something first. A missing 83(b) filing. A contractor who never signed an IP assignment. A cap table that doesn’t reconcile. A customer contract with a change-of-control clause nobody read closely.

None of that is fatal on its own.

What kills the deal is when it surfaces mid-diligence, in front of the person deciding whether to wire you money.

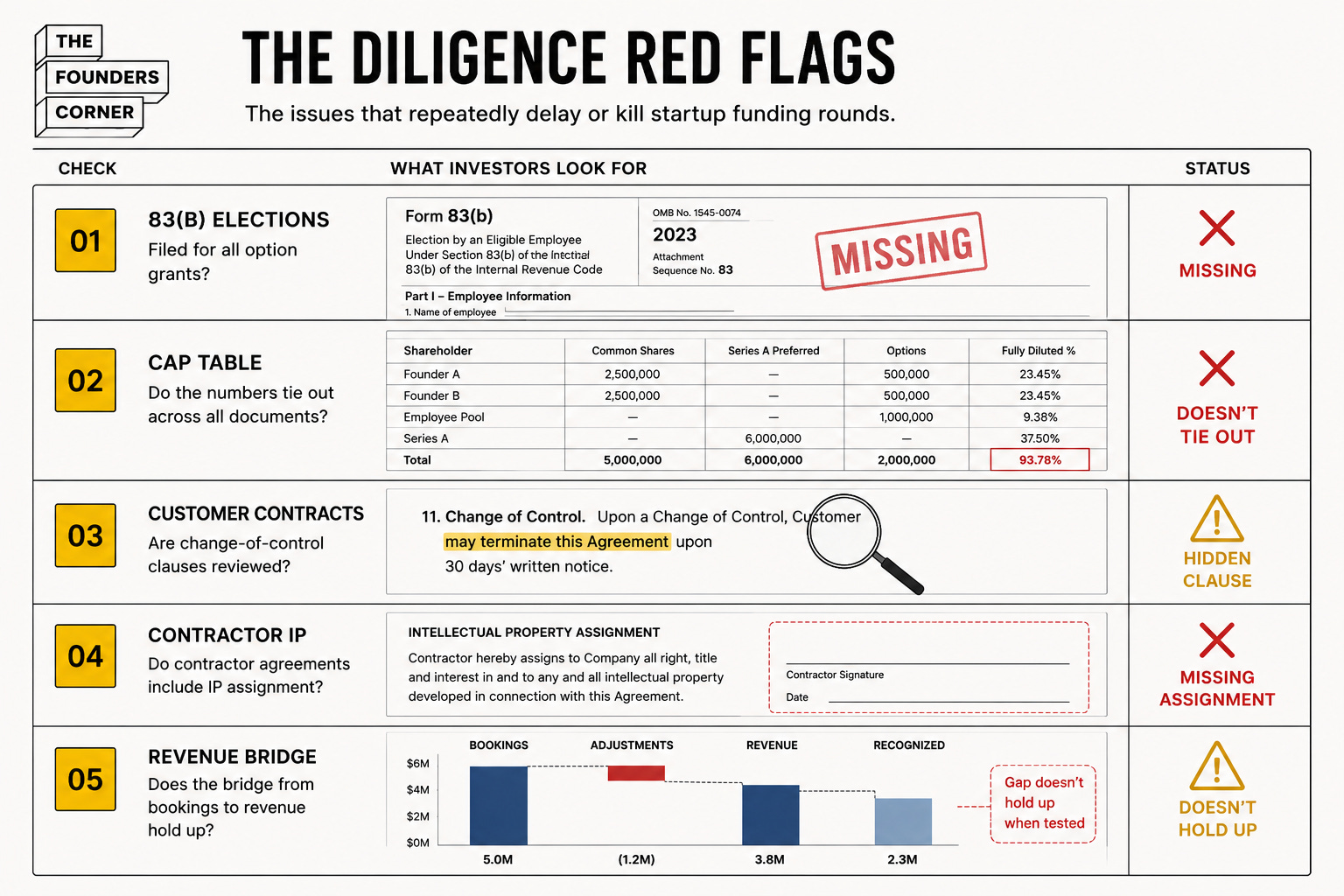

The numbers behind the collapse

4 to 10 weeks. That’s the standard window between term sheet and close.

A third of collapsed deals die from preventable cap table or documentation gaps. Not from the business changing.

The repeat offenders: missing 83(b) filings, cap table entries that don’t tie out, buried change-of-control clauses, contractor agreements with no IP assignment, a bookings-to-revenue bridge that doesn’t hold up when someone checks it.

Almost none of this is an investor trying to catch you.

It’s paperwork you’d have fixed in five minutes if you’d known to look.

Two founders get the same data room request.

One starts pulling documents in real time, finds three contractors who never signed IP assignments, and spends two weeks in reactive cleanup while the investor’s confidence quietly erodes.

The other already ran the audit weeks ago. The gaps are closed. The request lands on a folder, not a scramble.

Same company. Different outcome.

Here’s the eight-prompt system that gets you to the second founder.

Prompt 1: The diligence self-audit

Run this before you send a single document. It’s the same first pass a diligence analyst runs, pointed at your own company while you still have time to fix what it finds.

💬 Copy this prompt into Claude

I'm about to go through investor due diligence for a [STAGE] round.

Company: [ONE-SENTENCE DESCRIPTION]

Round size: [AMOUNT]

Act as a diligence analyst doing a first-pass structural review before

the formal process starts. Based on standard diligence practice at my

stage, walk through these five categories and tell me, for each one,

what a real analyst would ask for and what commonly goes wrong:

1. Corporate and cap table: incorporation documents, 83(b) filings,

option grants, cap table reconciliation, prior round documentation

2. IP and technical: assignment agreements for every founder, employee,

and contractor who touched the product; open-source license exposure

3. Financial: how bookings, billings, and recognized revenue relate to

each other, and whether that bridge is documented anywhere

4. Customer and commercial: contract terms, concentration risk,

change-of-control clauses, renewal terms

5. Team and employment: offer letters, equity vesting schedules,

any verbal agreements that were never formalized in writing

For each category, ask me direct yes/no questions that would surface a

real gap, not generic checklist items. Where I answer "I'm not sure,"

flag that as a priority to verify this week, not later.💡 Why this works: “Review my company for due diligence” produces a generic checklist. This produces the specific, categorized gap list an analyst would actually build, and it puts your uncertain answers at the top instead of the bottom.

If this is useful, it’s worth knowing it’s one piece of a bigger system.

The prompt above assumes you’ve already got a term sheet in hand and a story that holds together under scrutiny. That’s not a given. It’s the output of everything that happens earlier in the process, and we’ve built the same kind of copy-paste system for each stage:

You Just Got a Term Sheet. Do Not Sign It Yet.: the seven-prompt system for reading every clause and knowing exactly what to push back on before you get to this point

How to Build Your Fundraising Narrative With Claude: the five-prompt playbook for turning your raw story into the argument that gets you a term sheet in the first place

I Asked Claude to Reject My Pitch Until It Couldn’t. Then I Raised.: the adversarial system that finds the weak points in your story before an investor does

The Claude Guide Every Founder Should Run Before Fundraising: the nine prompts that replicate how modern VC firms screen your deck with AI before a partner ever opens it

I Made Claude Build My 13-Week Cash Flow Forecast: the same “raw files in, structured output out” pattern above, pointed at your cash position instead of your data room

Prompt 2: The cap table reconciliation

The highest-frequency failure point in early-stage diligence. Almost always an honest mistake, not a red flag.

A rounding error from your seed round. An option grant that never got formally documented. A SAFE that converted on the wrong terms.

None of it malicious. All of it reads as one if an investor’s lawyer finds it first.

💬 Copy this prompt into Claude

Here is my current cap table: [PASTE OR DESCRIBE YOUR CAP TABLE]

Here is my incorporation documentation and prior round terms:

[PASTE RELEVANT DETAILS - SAFE terms, conversion terms, option pool size]

Walk through this cap table line by line and check:

1. Does total ownership sum to exactly 100%, accounting for the

fully diluted option pool?

2. Do any SAFEs or convertible notes have conversion terms that

don't match what's reflected in current ownership?

3. Are there any option grants mentioned in board minutes or offer

letters that aren't reflected in the cap table, or vice versa?

4. Is the option pool sized and dated consistently with when it

was actually approved?

For anything that doesn't reconcile, tell me exactly what's

inconsistent and what documentation I'd need to pull to resolve it

before an investor's counsel finds the same issue.⚡ Run this a week before you expect a term sheet, not after. A cap table fix takes an afternoon when nobody’s watching. It takes a lot longer when it’s a redline in someone else’s document.

🔒 Two prompts down. Six to go before your data room is actually ready.

The self-audit and the cap table check tell you where the gaps are. They don’t close the ones underneath the ones you can see. Paid subscribers get the next six prompts in full, plus the tools that go with them:

✓ Prompt 3: The IP and contractor assignment sweep - builds the full list of everyone who has ever touched your codebase, product, or IP, cross-references it against your signed assignment agreements, and tells you exactly which gaps to close and in what order.

✓ Prompt 4: The customer concentration and contract risk map - scans your customer contracts for change-of-control clauses and revenue concentration risk, and gives you the specific renegotiation language to send before an investor’s call with your biggest customer surfaces it first.

✓ Prompt 5: The bookings-to-revenue bridge - documents exactly how your bookings, billings, and recognized revenue connect, so the financial story you told in the pitch still holds up when an analyst pulls the actual numbers apart.

✓ Prompt 6: The data room structuring prompt - takes whatever scattered documents you already have and organizes them into the standard sections a real investor data room expects, in the order they expect to review them.

✓ Prompt 7: The reference call prep - briefs your customer references on the specific questions an investor is likely to ask, so their answers and your pitch tell the same story.

✓ Prompt 8: The diligence Q&A simulator - runs a mock round of the specific follow-up questions your actual gaps are about to generate, so you’re answering them for the second time by the time a real analyst asks.

Paid subscribers also get:

✓ 60+ additional tools covering every other stage of fundraising and running a company: pitch deck screening, investor research and outreach, meeting prep, term sheet analysis, and data room management. The same tool stack this ARR workflow came from.

Prompt 3: The IP and contractor assignment sweep

Your product is only unambiguously yours if every person who built any part of it signed something that says so.

Founders almost always have this right for co-founders and full-time hires. It’s the contractor from year one, the freelance designer, the friend who “helped out for a few weeks,” that gets missed.

💬 Copy this prompt into Claude

Keep reading with a 7-day free trial

Subscribe to The Founders Corner® to keep reading this post and get 7 days of free access to the full post archives.