The 6 Claude prompts that change what you walk into the room with

Most founders spend their prep time on the pitch. The founders who close rounds spend it on the investor. Here’s the six-prompt meeting system that changes what walks into the room with you.

A VC meeting is not where the decision gets made.

This is the thing most founders don’t understand, and it explains why so many good companies don’t get funded.

By the time you sit down across from an investor, they’ve already formed a view. They read your email. They looked at your deck. They Googled your co-founder. They checked your LinkedIn. They read the one article you wrote three years ago that you’d rather they hadn’t. They looked at the three companies in their portfolio that are adjacent to yours and thought about whether you’re a threat, a complement, or irrelevant.

They walked into the room with a thesis about your company.

The meeting confirms it or contradicts it.

Founders who prepare for the investor (who know what they’ve said publicly about your market, which of their portfolio bets are relevant to you, what they’re likely to push on, and how to frame the same company differently for different funds) confirm a positive thesis before they’ve answered the first question.

Founders who prepare for the performance (who practise their slides, memorise their TAM, run through their answers for the hundredth time) walk into an unknown room and hope for the best.

The prompts below are the preparation system that changes what you walk into the room with.

The math that makes every meeting count

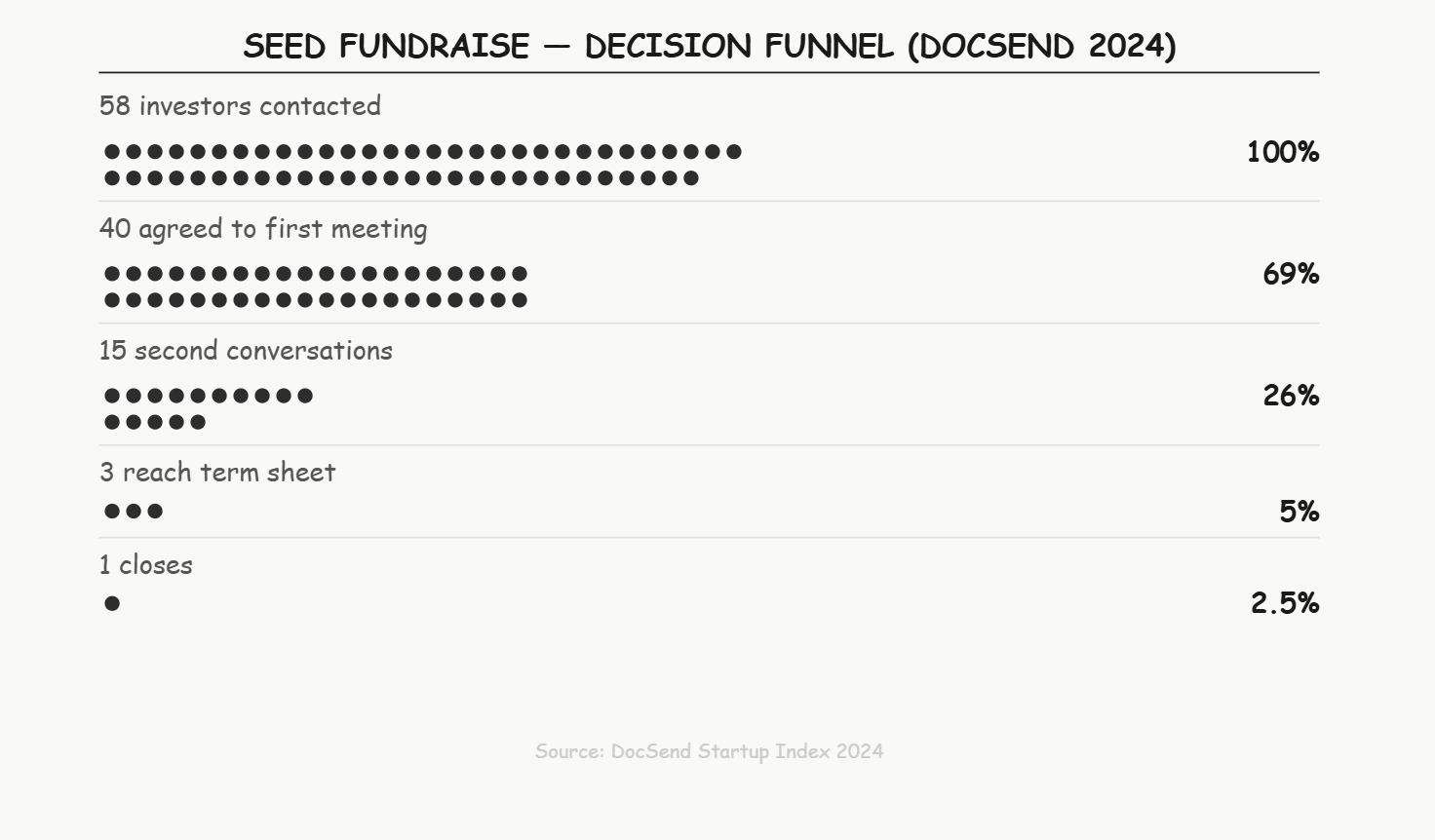

Here’s the DocSend data from 2024 on a typical seed fundraise.

The average founder contacts 58 investors. 40 agree to a first meeting. 15 reach a second conversation. 3 or 4 reach term sheet stage. 1 closes.

That’s a 2.5% conversion rate from first meeting to close.

Which means each of those 40 meetings matters enormously, and most founders treat them as roughly the same. Same pitch. Same story. Same framing. The investors doing the evaluating are not the same. A fund that has made three infrastructure bets evaluates you differently from one that’s actively looking for its first.

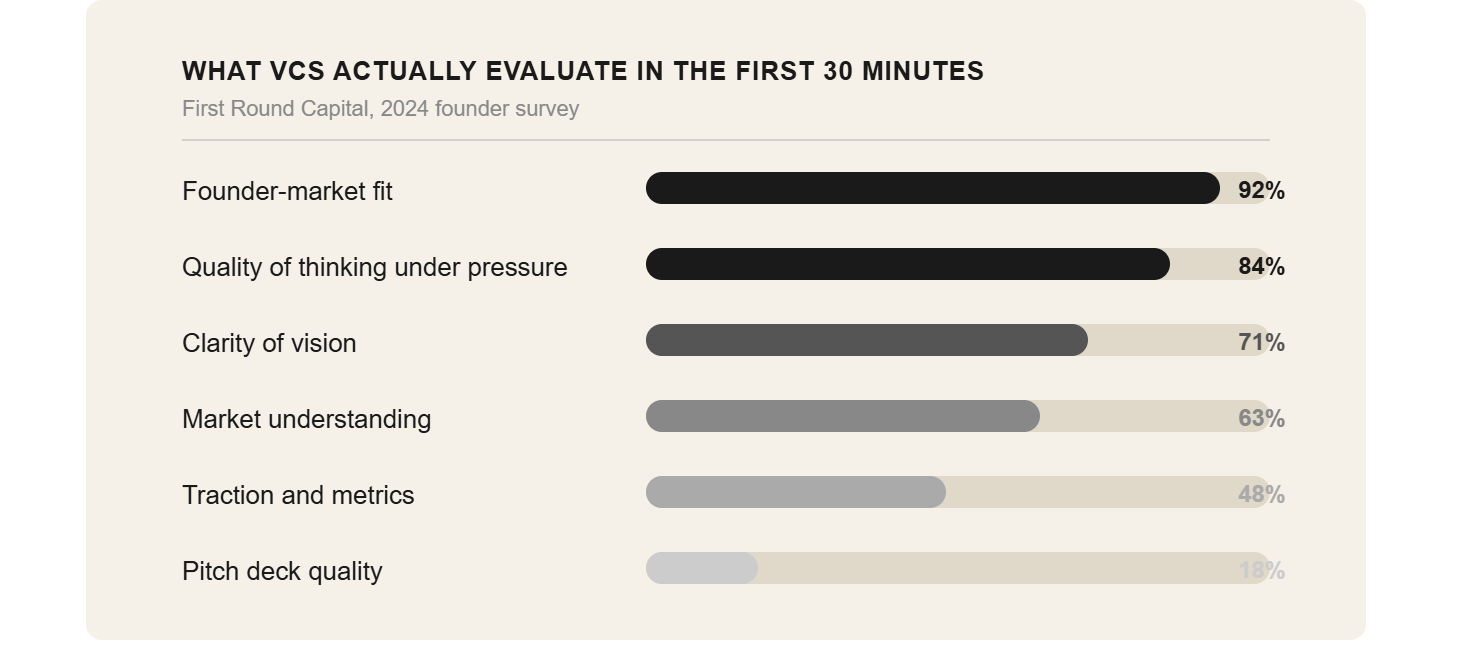

What a VC is actually evaluating in your first 30 minutes

Not your deck. Not your market size slide.

First Round Capital’s 2024 founder survey asked investors what they’re primarily assessing in first meetings. The top answers:

Notice what’s at the top: founder-market fit, and quality of thinking under pressure. Both of those are evaluated from how you answer questions, not from your slides.

The best preparation you can do is not perfect your slides. It’s know what questions are coming, know why they’re being asked, and know how to answer them in a way that demonstrates the thinking these investors are specifically looking for. That preparation looks different for every investor.

Prompt 1: The meeting agenda builder

Before you prepare your pitch, prepare for their perspective.

This prompt takes the investor’s name, fund, and any public context you have (recent investments, articles they’ve written, talks they’ve given) and builds a structured briefing on what they’re likely to focus on in the next 30 minutes.

The prompt:

I have a first meeting in [X days] with [INVESTOR NAME] at [FUND NAME].

Here is what I know about them and their fund:

- Fund stage and focus: [e.g., seed/early-stage, B2B SaaS, infrastructure, consumer]

- Recent investments I know about: [3-5 recent portfolio companies]

- Anything they've written or said publicly: [paste any relevant quotes, article summaries, or conference talk notes]

- Portfolio companies relevant to my space: [any overlap or adjacent bets]

Here is a brief description of my company:

- What we do: [one paragraph]

- Stage and traction: [round size, ARR or users, key metrics]

- Why now: [the market shift that makes this the right moment]

Based on this, please do three things:

1. Build a 'meeting agenda from their perspective'. Based on their known thesis and portfolio,

what are they most likely to spend the first 30 minutes on? What categories of question

will they focus on, and why?

2. Identify the one thing about my company that most directly maps to something they've

publicly said they care about. This is the anchor I should return to throughout the meeting.

3. Flag the one thing about my company or stage that is most likely to create hesitation

for this specific investor (not generic VC concern, but the concern that maps to their

known investment criteria. I should walk in knowing what this is.Run this before any other prep. The output tells you what room you’re actually walking into, not the generic VC meeting you’ve been preparing for.

You’re one prompt in. The next five (the questions they’ll ask, the narrative pivot, the questions to ask them, the signal reader, and the 24-hour follow-up builder) are for paid subscribers below.

🔒 The rest of the system is for paid subscribers

Prompt 1 tells you what the investor is thinking. Prompts 2–6 tell you exactly what to say, ask, and send.

✓ Prompt 2: The 7 questions they’ll ask. Specific to this fund’s thesis, stage, and known portfolio gaps. Not generic VC questions; the ones this investor is likely to ask you, based on what they’ve said publicly and what their portfolio tells you they believe.

✓ Prompt 3: The narrative pivot. How to frame your company for this specific investor, not a generic pitch. The same company can be “AI-native infrastructure” for one fund and “PLG SaaS at seed stage” for another. This prompt tells you which frame lands best and why.

✓ Prompt 4: The questions to ask them. The three questions that demonstrate preparation, reveal the fund’s actual decision process, and shift the dynamic from pitch to conversation. Includes the one question that tells you whether this investor will actually move.

✓ Prompt 5: The signal reader. What investor behaviour during the meeting actually signals: leaning in vs. leaning back, asking about the team vs. asking about competitors, the note-taking tells. Tells you how to read the room in real time and adjust.

✓ Prompt 6: The 24-hour follow-up builder. The follow-up email that references something specific from the conversation, reinforces the two points you want to stick, and proposes a clear next step. The move that separates founders who advance from those who wait.

✅ Instant access to 50+ other tools and walkthroughs we’ve already built: outreach sequences, term sheet explainers, data room checklists, follow-up frameworks, covering the entire fundraising process from first contact to close.

Prompt 2: The 7 questions they’ll ask

This isn’t a list of common VC questions. It’s the seven questions that this specific investor, with this specific thesis and portfolio, is most likely to ask you.

Keep reading with a 7-day free trial

Subscribe to The Founders Corner® to keep reading this post and get 7 days of free access to the full post archives.