The Document That Is Killing Your Series A (And You Have Already Signed It)

You agreed to terms you did not fully understand. An investor is about to explain them to you

You are sitting across from a Series A investor. The conversation is going well. They ask about the cap table.

You pull it up.

There is a moment where their expression does not change but something shifts. They ask one question about the SAFE from eighteen months ago. You answer it. They write something down and move on.

Three weeks later they pass. The email says the round is not the right fit for the fund right now.

It was the cap table.

It is almost always the cap table.

Not because it was fraudulent. Not because you did anything wrong. Because you had agreed to terms in earlier rounds without fully understanding what they would look like to the next investor. A conversion cap that implied an unrealistic valuation. A pro-rata clause that gave an existing investor the right to take half the new round. An option pool agreed at the wrong time, diluting founders instead of investors.

Small decisions, made under time pressure, that compound into a structure the next investor cannot work with.

The cap table is the record of every financial decision you have ever made about your company. Most founders treat it as admin. The investors reading it treat it as signal.

What the Cap Table Is Actually For

A cap table has two jobs.

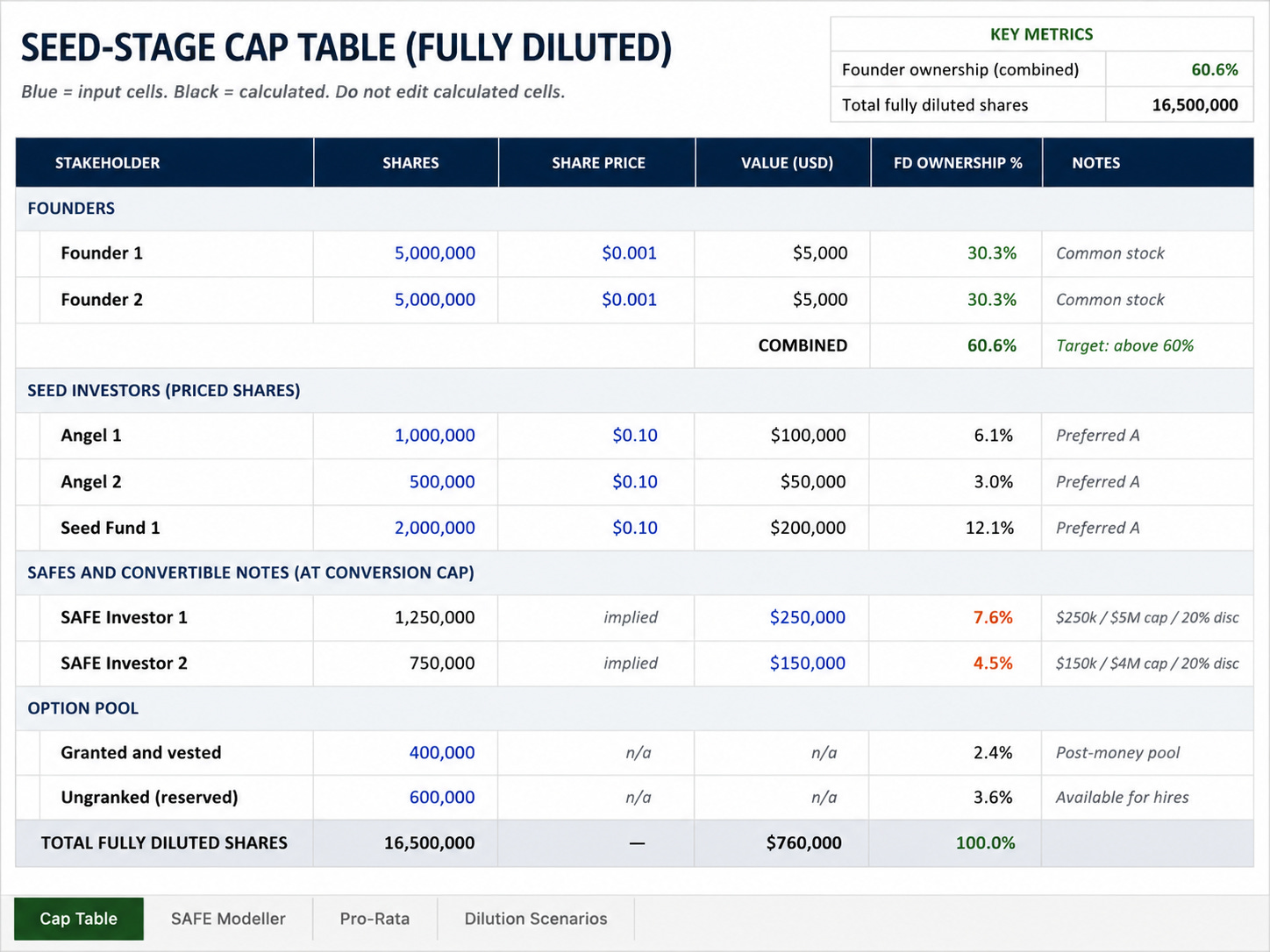

The first is to track ownership. Who owns what, on what terms, at what stage.

The second job is more important and almost never talked about. It tells the next investor exactly how the round before them was structured and what that says about how you negotiate.

Founders who understand this build their cap table with the next investor in mind, not just the current one. Every SAFE they sign, every option pool they agree to, every pro-rata right they grant, they are thinking about how that decision looks in twelve months when a new investor is reading it.

Founders who do not understand this agree to terms that seem reasonable in the moment and discover the problem during Series A due diligence, when it is too late to undo them without significant friction.

The decisions that matter most are not complicated. They are just not explained to founders before they sign.

The Three Decisions Most Founders Get Wrong

Most founders know they have a cap table. Very few know what is actually in it.

These three decisions are where the damage happens.

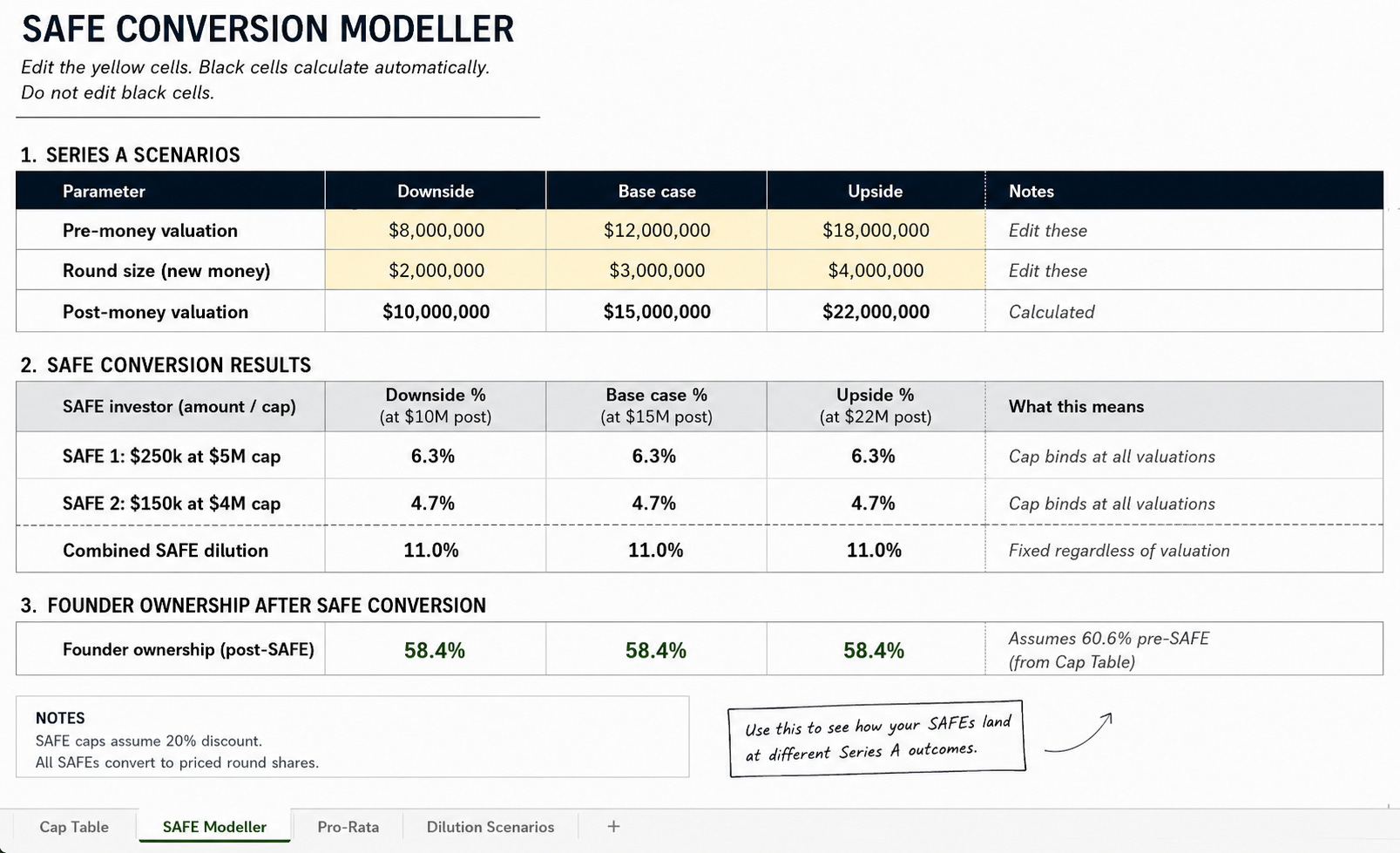

The SAFE conversion cap. A SAFE converts into equity at your next priced round, and the conversion cap determines what valuation it converts at. If you raised a SAFE at a $5M cap eighteen months ago and you are now raising a Series A at a $20M pre-money valuation, the SAFE investor converts at $5M, takes a large chunk of equity, and the effective price paid per share is far below what the Series A investor is paying for the same class of shares.

Series A investors look at this and either price the dilution into their offer, reduce the round size, or pass.

The fix is not complicated. Model the conversion before you agree to the cap. Know what the SAFE looks like at three different Series A valuations. Make the decision with that information, not without it.

The option pool. Most early-stage term sheets include a clause requiring founders to establish or expand the option pool before the investment closes. This sounds reasonable. The problem is timing.

If the option pool is created before the pre-money valuation is set, the dilution comes entirely from the founders and existing shareholders. If it is created after, the dilution is shared across all shareholders including the new investor. The difference in founder ownership between these two structures can be four to eight percentage points by Series A.

Every founder who has been through a Series A knows this. Most founders raising their seed round do not.

Pro-rata rights. Giving an investor the right to participate in future rounds at their current ownership percentage sounds like a small concession when you are trying to close a seed round quickly.

By Series A, if your seed investors hold pro-rata rights and exercise them, they can collectively take 20 to 30 percent of the new round before the lead investor has put a single dollar in. Series A investors who see this do not celebrate it. They negotiate around it, and you lose leverage in the process.

What a Healthy Seed-Stage Cap Table Looks Like

There is no universal answer. But there are patterns that Series A investors consistently respond well to.

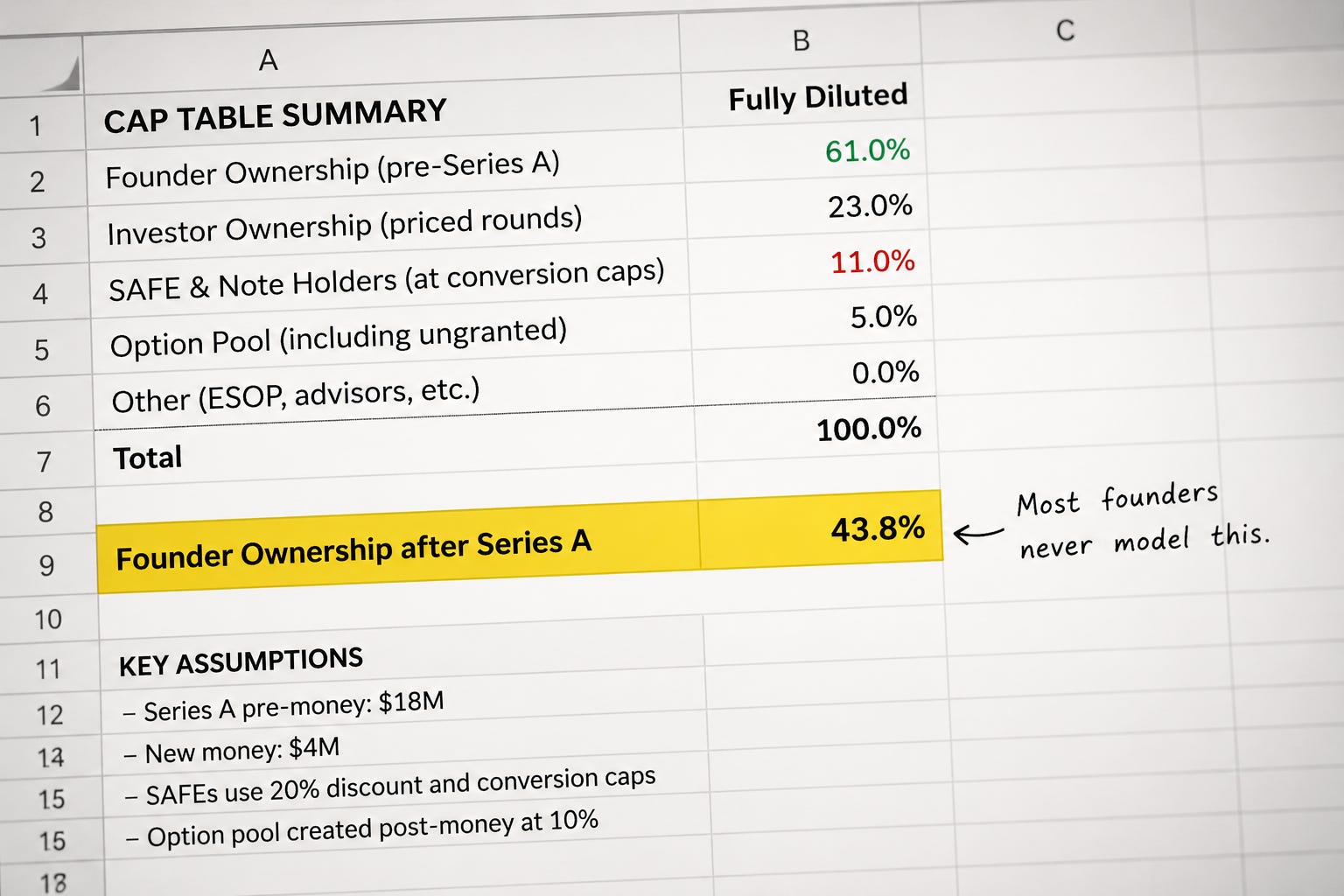

Founder ownership above 60 percent combined at the point of closing a seed round. It tells the next investor that you did not give away control early and that there is enough equity runway to recruit senior talent and complete another two rounds before founders are below the threshold where their incentives start to misalign.

An option pool of 10 to 12 percent, created post-money rather than pre-money. Not 20 percent because someone told you that is what investors expect. Sized for the actual hires you plan to make in the next 18 months.

SAFE conversion caps that reflect the realistic valuation trajectory. If you are raising a seed at $2M and you believe you will be at $8M to $12M pre-money at Series A in two years, the cap should sit somewhere in that range. Not the current valuation, not an aspirational number 10x above it.

A small number of seed investors, each with pro-rata rights that are conditional rather than unconditional. Conditional pro-rata rights, which vest only if the investor has supported the company actively, are increasingly accepted and worth pushing for.

The Problem With Spreadsheets You Did Not Build

Here is something that happens more than anyone admits.

Most founders manage their cap table in a spreadsheet they did not create, downloaded from somewhere, updated piecemeal as new rounds closed. The formulas are partially broken. The fully diluted share count is wrong because someone forgot to include the convertible notes. The option pool shows granted shares but not unvested ones.

This is the document they send to Series A investors when asked for the cap table during diligence.

The investor has seen thousands of cap tables. They know immediately when something does not add up. They start asking questions. The founder answers them as best they can.

And the investor’s confidence in the founder’s command of their own business starts to decay.

A clean cap table, maintained rigorously, with a one-page summary that explains the structure in plain English, is one of the most credible signals a founder can send.

It says: I know my business. I know the terms I agreed to. I can defend every number on this page.

How to Audit Your Cap Table Before You Raise

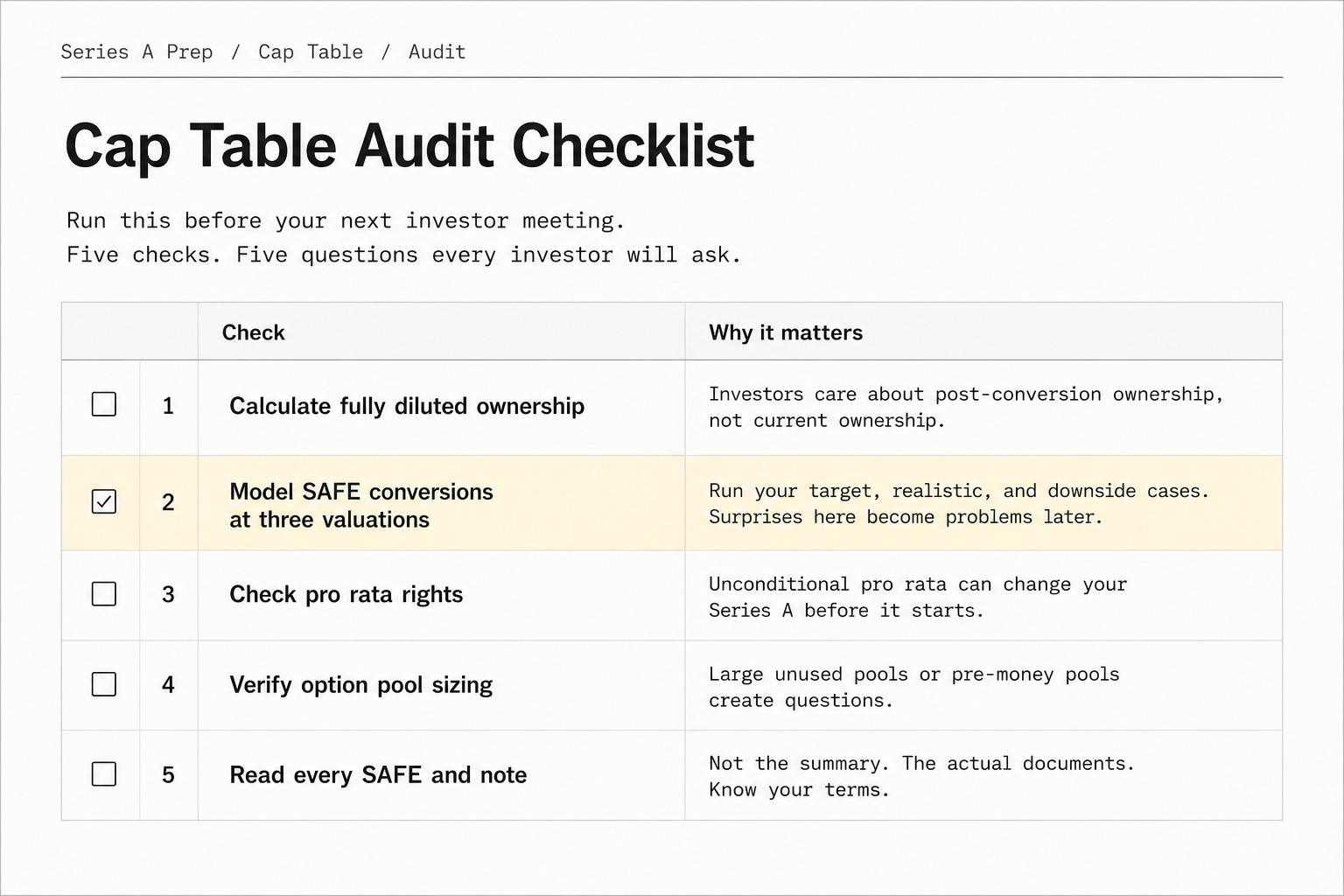

Before your next fundraising conversation, run through these five checks.

Calculate your fully diluted ownership. Include issued shares, all SAFEs and convertible notes at their conversion caps, the full option pool including ungranted options, and any warrants. The number that matters is not your current percentage. It is your percentage after everything converts.

Model your SAFE conversions at three valuations. Take the valuation you are hoping for, the valuation you realistically expect, and a valuation 30 percent below that. See what each early SAFE holder owns at each scenario. If the answer surprises you in any of those scenarios, you need to understand it before an investor asks.

Check who holds pro-rata rights and whether they are conditional or unconditional. If you have investors with unconditional pro-rata rights holding more than 25 percent of your seed round combined, model what happens if they all exercise in your Series A.

Verify your option pool against your actual hiring plan. If you are 18 months from a Series A and your option pool has 40 percent ungranted, you either have too large a pool or you are not hiring as aggressively as your cap table assumes. Either creates a question.

Read every SAFE and note you have issued. Not the summary. The actual document. Look at the most favoured nation clause. Look at the conversion mechanics. If you cannot explain every line to an investor without looking at the document, you do not know your own terms.

The Conversation Most Founders Avoid

There is a version of the cap table conversation that founders dread and therefore delay.

It is the conversation with their existing investors about cleaning something up before the next round.

A SAFE with an MFN clause that no longer reflects what you would agree to today. A pro-rata right that will become a problem at Series A. An investor who holds a small stake but has board observer rights that a lead investor will not want.

These conversations are uncomfortable.

They are far less uncomfortable before a Series A than during one.

A Series A investor who discovers structural issues during diligence does not have the patience or the incentive to help you fix them. An existing investor who is asked six months before a raise to amend a term for the good of the company’s future has a clear incentive to cooperate.

The founders who raise Series A rounds cleanly are not the ones with the cleanest cap tables by accident. They are the ones who spent time in the twelve months before their raise identifying the problems and addressing them proactively.

If you are raising in the next 90 days, these are the issues that will do the most work alongside this one.

→ The Most Dangerous Document a Founder Will Ever Sign - the full term sheet deep dive, the clauses that matter most and the ones that follow you for years. Read this before you sign anything.

→ The Data Room That Does Not Lose Deals at the Last Minute - what to send, how to structure it, and the audit to run before every send.

→ Before You Pitch: The Negotiation Secrets Investors Do Not Want You to Know - how to enter any funding conversation with leverage rather than gratitude.

The Cap Table Audit Workbook

Most cap table tools tell you what you own.

This one tells you what your cap table looks like to the next investor.

The Cap Table Audit Workbook is a working document built for one purpose: identifying and fixing the structural issues in your cap table before a Series A investor finds them for you. Open it before your next fundraising conversation. Work through each tab. You will either confirm your cap table is clean or find the problem in time to address it.

What’s inside:

✅ Fully diluted ownership calculator - input your shareholders, SAFEs, notes, and option pool and the workbook calculates your fully diluted table automatically

✅ SAFE conversion modeller - enter your target Series A valuation and see exactly what every SAFE and note converts to, in shares and percentage, across three scenarios

✅ Dilution scenario builder - runs your optimistic, realistic, and downside valuations side by side so you can see founder ownership at each outcome through Series A and Series B

✅ Pro-rata impact calculator - shows the effect of all pro-rata right holders exercising into your Series A before the lead investor commits

✅ Option pool sizing tool - sizes your pool against your actual 18-month hiring plan rather than an arbitrary percentage

✅ Cap table clean-up brief template - the structured document you send to an existing investor when you need to renegotiate a term before the next round

✅ Annotated example cap table - a worked example showing what a clean seed-stage cap table looks like, with commentary on every decision

This is what a paid subscription to The Founders Corner gets you every week.

Not frameworks to screenshot and store. 50+ tools you open, use, and walk away from with something concrete, built for the decisions founders are actually making.

The Cap Table Audit Workbook is available exclusively to premium subscribers of The Founders Corner.