McKinsey Just Interviewed 4,000 of Your Customers. Here Is What They Found.

The rules of B2B selling changed two years ago. Most founders building B2B companies have not noticed.

A B2B founder in my portfolio spent eighteen months building a sales motion around a single channel. Great product. Strong ICP. Disciplined outbound. The pipeline looked fine.

Then two enterprise deals switched suppliers inside the diligence window. Not to a competitor with a better product. To a competitor with a better buying experience. Faster responses. A self-serve demo. A pricing page that did not require a sales call.

He had built for buyers that no longer existed.

I have seen this pattern more times than I can count. A founder optimises the thing they can see - the pitch, the product, the outbound sequence - and misses the thing they cannot see: the buying experience happening on the other side of the screen before they ever get on a call.

McKinsey has just published the tenth edition of its Global B2B Pulse Survey. Nearly 4,000 decision-makers across 13 countries. I read it cover to cover because I sit on boards of B2B companies and I wanted to understand what the people they are trying to sell to are actually doing.

The headline is not about AI or omnichannel or personalisation, though all three feature. The headline is about the floor.

Everything the industry spent the last decade building toward is now simply the minimum required to stay in the game. The capabilities that used to be a competitive advantage - digital channels, e-commerce, seamless handoffs between sales and self-serve - are now the price of admission. What used to be the ceiling is now the floor.

For founders building B2B companies in 2026, this is not an enterprise problem. It is a go-to-market problem that starts on day one.

What Buyers Actually Do Now

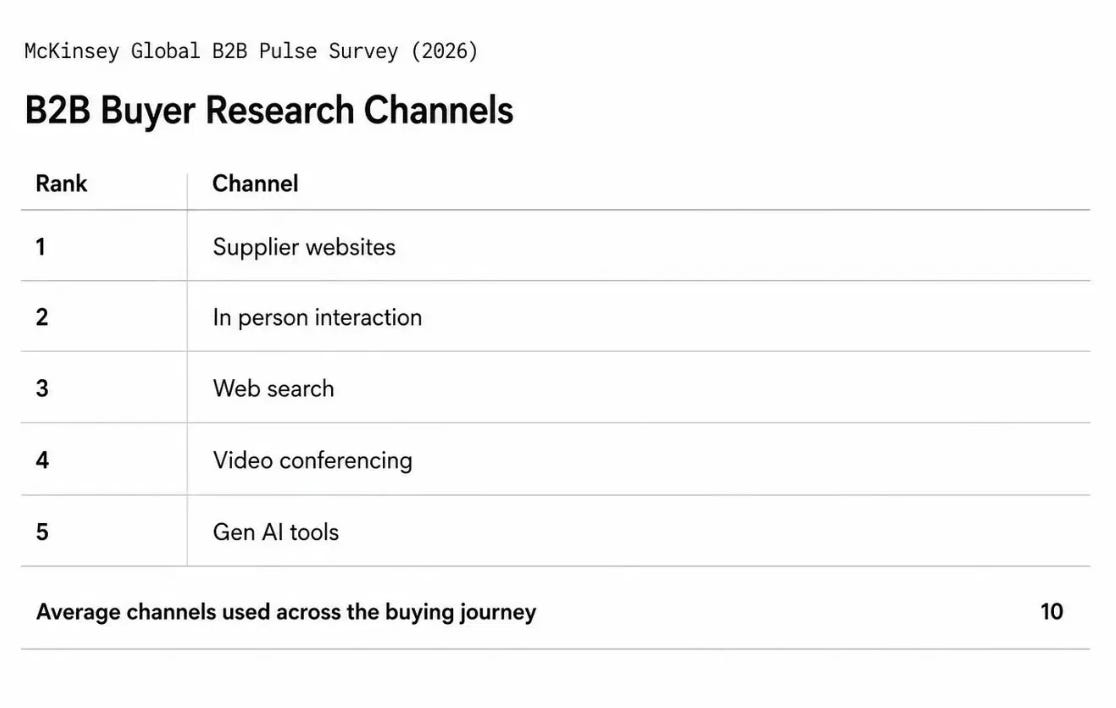

The first number every B2B founder needs to know: buyers now use an average of ten channels across the purchasing journey and expect seamless movement among them.

Ten channels. Not one or two. Ten.

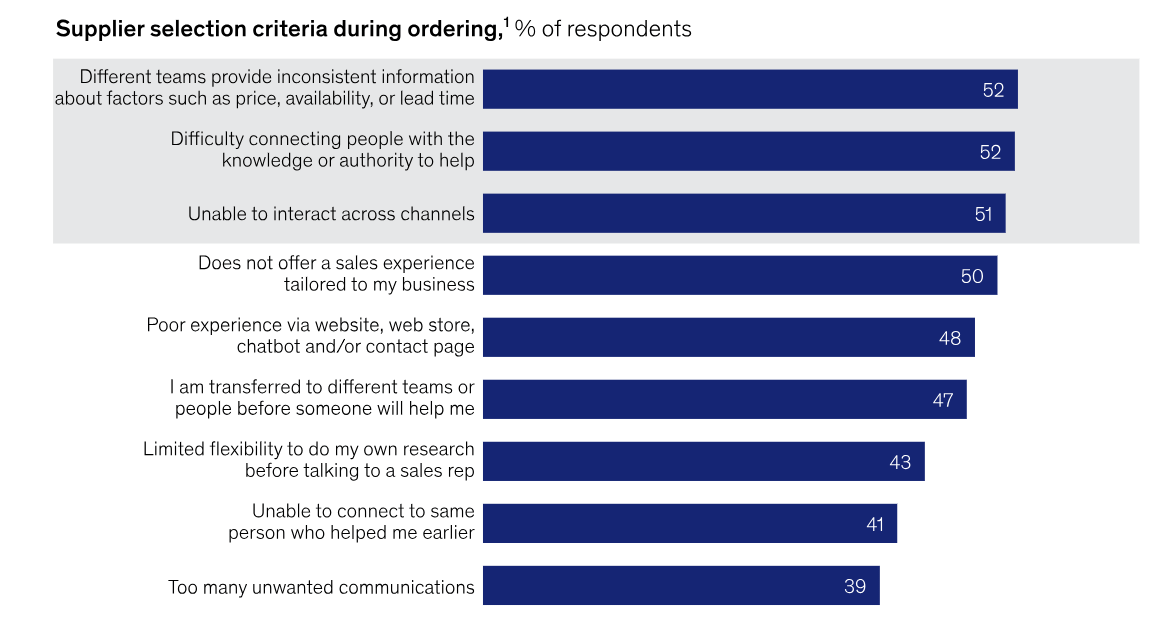

Your outbound sequence, your demo call, your pricing page, your LinkedIn presence, your case studies, your G2 profile, the response time on your email, how quickly your champion can get internal approval - all of it is part of the same buying experience. Buyers are moving across all of these before they have spoken to a single person on your team. And if any one of them breaks the experience, inconsistent information and lack of knowledgeable support are now the leading drivers of supplier switching.

The second number: seventy-one percent of B2B companies now offer e-commerce, and among those, roughly one-third of revenue now flows through digital channels.

Self-serve is not a feature. It is where the money is moving.

The Gap Between Winners and Everyone Else

This is where the data gets consequential.

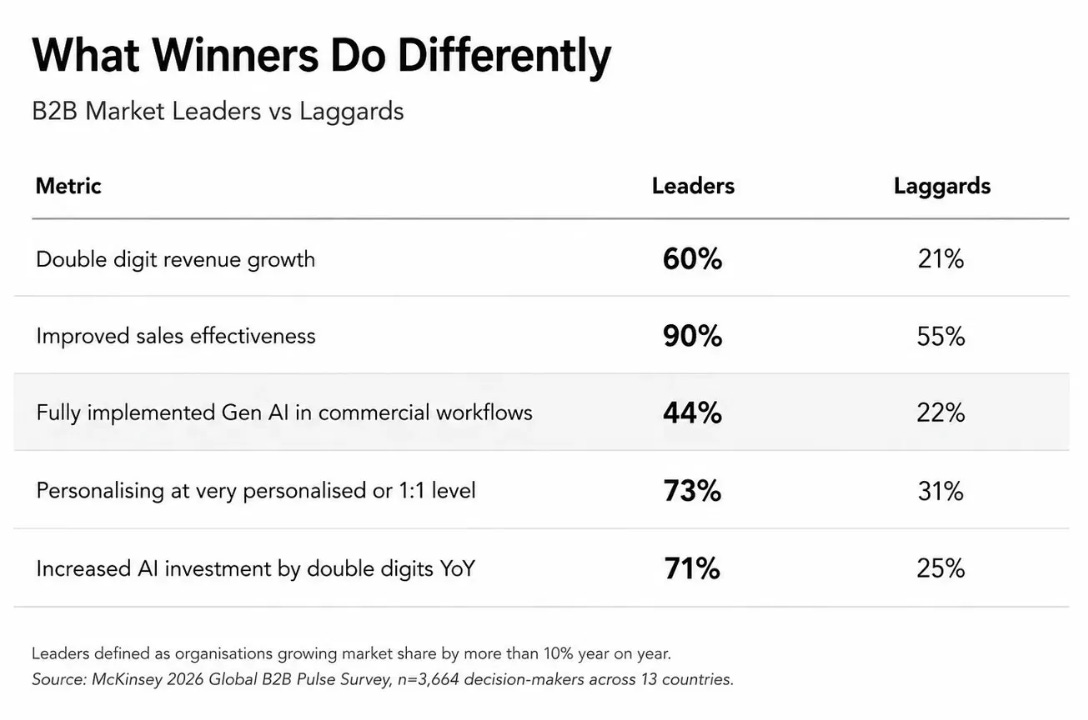

Sixty percent of market leaders - defined as organisations growing market share by more than ten percent year on year - reported double-digit revenue growth in 2025, compared with just 21 percent of laggards.

That is not a marginal difference. It is a structural one. I see this gap in my portfolio. The companies pulling away are not doing so because they have a better product than their peers. They are doing so because they have built a commercial motion that reflects how buyers actually behave now, not how they behaved three years ago.

Ninety percent of leaders said sales effectiveness has improved, versus 55 percent of lower-performing peers. The same technology is available to both groups. The same channels exist. What separates them is not access - it is how coherently those capabilities are built into the commercial model.

McKinsey’s data points to three specific things the winners are doing that most early-stage founders are not. I will get to all three in detail below. But first, the number that should stop every founder reading this.

Leaders were twice as likely as laggards to have fully implemented generative AI in their commercial workflows. Seventy-three percent of winners were personalising at very personalised or one-to-one levels, compared with 31 percent of laggards. And the companies growing fastest have made one person accountable for the pipeline end to end - not a committee, not a shared function. One person.

The gap is not narrowing. It is structural. And it starts earlier than most founders think.

If you are building a B2B company and thinking about your go-to-market, these are the issues that will do the most work alongside this one.

→ The GTM Mistake That Kills More Startups Than Bad Products - the sequencing error most founders make before they have found a repeatable motion, and how to fix it

→ What Separates Founders Who Scale From Founders Who Stall - the six frameworks behind every B2B company that builds a commercial engine that compounds

→ The Fundraising Cheat Code Most Founders Discover Too Late - how to use go-to-market traction as the narrative anchor that closes institutional rounds faster

The Three Things Winners Are Doing That Most Founders Are Not

The McKinsey data points to three specific places where the gap between leaders and laggards is widest. Here is my read on what each of them actually means for a founder at your stage - not for an enterprise commercial team.