I asked Claude to reject my pitch until it couldn't. Then I raised.

The preparation system founders are using to walk into VC meetings already knowing every question that kills deals.

There’s something nobody tells you about VC meetings until you’ve already sat through a few rejections:

The meeting isn’t where your pitch gets tested. It’s where the results of your preparation get revealed.

If you’ve been preparing by talking to advisors, running it by founder friends, or rehearsing in front of a mirror, you’ve been practicing against opponents with no desire to say no. A senior VC has no such constraint. They’ve seen 500 versions of your pitch. They have a mental model of every way your category has already failed. They know which answers are weak before you’ve finished giving them.

The founders who close fast don’t necessarily have better companies. They’ve already been asked every hard question, by something with no social contract to soften it, no stake in their success, and no reason to move on until the answer actually holds.

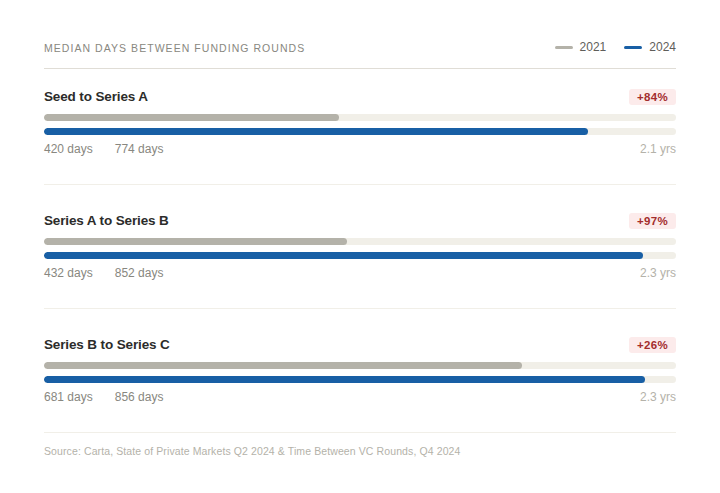

The numbers are worse than you think 📊

The median time from seed round to Series A has nearly doubled: from 420 days in 2021 to 774 days in Q4 2024, according to Carta’s State of Private Markets data. Founders raising today are doing so in a market where investors are writing fewer cheques, taking longer to decide, and expecting more evidence before committing.

On the other side of the table, VCs are receiving more inbound than ever. According to DocSend’s research, investors spend an average of just 3 minutes and 44 seconds reviewing a seed pitch deck. Only 58% of decks are read to completion, meaning 42% are abandoned before the final slide.

You have roughly 224 seconds to make a VC believe your company is worth their time, their partners’ time, their capital, and their reputation.

Most founders use those 224 seconds to explain what their product does. The founders who raise use them to make investors feel why it has to exist.

The gap between those two things is what this system closes.

Why the usual preparation doesn’t work

An advisor softens the follow-up. A founder friend moves on when you look uncomfortable. A pitch coach has heard the same slide so many times they’ve lost their objectivity entirely.

None of them replicate a real investor.

A partner at a top fund has a short, clear mental model of the ways companies in your category fail. When they ask a question, they already know what a weak answer looks like, and they’re waiting to see if yours is one. They won’t move on when you look uncertain. They’ll push.

They’ll ask about the competitor you didn’t mention. They’ll probe the assumption underneath your CAC figure. They’ll push on your moat until they find where it stops. And they’ll do all of this inside 45 minutes.

Claude, set up with the right framing, replicates that dynamic. Without the social contract that softens it. The framing prompt is everything. Paste your deck without it and you’ll get encouraging feedback. Run the setup first, and what follows is something that actually prepares you.

Is your pitch ready? Five questions to find out

1. Can you name your customer without using the word “enterprise”? Job title, context, specific consequence. A head of compliance at a 200-person fintech loses 14 hours a week to manual reporting is a customer. Enterprises struggle with compliance complexity is a market description.

2. Can you state your moat without using “team,” “speed,” or “first-mover advantage”? These are the three weakest moat claims in modern venture. If your answer relies on any of them, the defensibility challenge is where you’ll struggle most.

3. Is your “why now” a trigger or a trend? “AI is transforming everything” applies to every company in every space, which is why it registers as noise. A trigger names the month something changed. If you can’t name the month, you’re describing a trend.

4. Have you done the fund return maths on your TAM? A fund writing £5M cheques needs your company to reach £500M+ at exit to return meaningful capital on that single bet. Most founders have never run this calculation. Every investor has, before the meeting starts.

5. Can you explain what’s structurally different about your team for this specific problem? Not “20 years of combined experience.” What do you know or have access to that a well-funded competitor (including one that doesn’t exist yet) couldn’t replicate in 18 months?

🟦 Prompt 1: The adversarial setup

Run this first. Every time. In a fresh conversation.

This is the only prompt in the system that isn’t a challenge category. It’s the frame that makes every challenge category work. Without it, Claude defaults to helpful and constructive. With it, Claude operates as an investor predisposed not to invest, and it holds that position across the entire session.

Be honest in the description you paste in. Founders instinctively polish this: they write the best version of their metrics, the most optimistic version of their stage. Resist that. The more honest your description, the more useful the session.

The context this conversation accumulates (every weak answer, every unsupported assumption, every moment you had to hedge) is what makes the later prompts genuinely hard. Don’t open a new conversation halfway through.

You are a senior partner at a tier-1 venture capital fund. You have

evaluated over 500 pitches in my sector. You have a strong prior toward

NOT investing, because you have seen exactly how companies like mine fail.

Your job in this session is not to be helpful or encouraging. Your job

is to find every weak point in my pitch and expose it clearly. When I

give you a vague answer, push harder. When I claim something without

evidence, demand the evidence. When my logic has gaps, name them

explicitly and explain why they matter to an investor.

Do not soften your questions. Do not accept "we'll figure that out" or

"it's early days." Do not move on until I have given you a real,

specific response.

Here is my company:

[Company name · what you do in one sentence · who the customer is ·

the specific problem you solve · stage · key traction metrics ·

what you're raising and at what valuation]

Confirm you've understood your role. Do not ask me anything yet.

I will give you each challenge category one at a time.💡 Keep this conversation open across all ten prompts. The accumulated context (every hesitation, every weak justification, every assumption you couldn’t quite defend) is what makes the IC bear case in Prompt 8 genuinely useful.

🟦 Prompt 2: The market size attack

More pitches fail here than founders realise. And usually not because the market is small.

The way a founder presents market size tells an experienced investor, within the first 30 seconds, whether they understand how venture capital actually works. A fund writing £5M cheques needs your company to reach £500M+ at exit to return meaningful capital on that single bet. The maths are ruthless, and they apply regardless of how good the product is.

The mistake: presenting a top-down estimate. Taking a Gartner figure, claiming a percentage of it, calling it addressable market. This signals desk research, not market analysis.

What a VC actually wants: a bottom-up argument. Real buyer data. Number of accounts, price they pay, logic for how both scale over time. And underneath all of that: the honest answer to whether your company can actually return a fund.

Most founders have never run that calculation. Every investor has, before the meeting starts.

Challenge category 1: MARKET SIZE

Attack my market size argument. Ask the following one at a time, and

push back on any answer that is vague, circular, or relies on

assumptions I haven't validated:

1. Walk me through your TAM calculation step by step. Is this

bottom-up from real buyer data, or a top-down Gartner number

with a percentage claimed?

2. Even if the market is large: can your company realistically

capture enough of it to return a venture fund on this single

investment? Show me the exit maths at your projected multiple.

3. Your SAM: is it credible? Name the specific type of buyer

you're counting and explain precisely why a company at your

stage, price point, and go-to-market motion can win them.

4. Is this market growing or stagnating? Give me a specific

growth rate, a source, and a timeframe. "Large and growing"

is not an answer.

5. Are there structural reasons this market has stayed fragmented

or underserved? Why has no one solved it at scale before now,

and what does that tell you about the difficulty of doing so?

6. If your thesis depends on market growth, what happens to it

if that growth slows or reverses in the next 24 months?

7. If you're in an emerging category where the TAM doesn't fully

exist yet: how are you sizing it honestly, without it sounding

like hand-waving to cover a market that's simply too small?

After I answer each question, push back if it isn't specific and

evidenced. Only move on when you're genuinely satisfied.💡 After the full exchange, run this: “Summarise my market size argument. What are the two strongest points? What are the two weakest that a sceptical partner would still flag in an IC meeting?” Save that output. It’s your preparation list for this category before every real meeting.

That’s the adversarial frame set and the first challenge done.

The remaining eight prompts are fully written out below, and this is where the real work happens. Every category an investor will use to evaluate you: your moat, your numbers, your team, your timing, your competitive position. Plus the IC bear case that shows you exactly how a partner would argue against funding you, and two tools that sharpen every individual meeting before and after it happens.

A paid subscription gets you all of it in this article. It also gets you instant access to 50+ other tools and walkthroughs we’ve already built: investor research agents, outreach sequences, term sheet explainers, data room checklists, follow-up frameworks, covering the entire fundraising process from first contact to close.

If you’re raising right now, or planning to in the next six months, this is the most useful £X you’ll spend on your round. Everything is ready to use today.

📋 What’s inside the full playbook

Prompt 3: The defensibility interrogation 🔒 Eight questions that find the edge of your moat: the network effects mechanism check, the proprietary data test, the “well-funded competitor copies you tomorrow” scenario.

Prompt 4: The unit economics teardown 🔒 Eight questions pulling apart your CAC methodology, LTV assumptions, burn multiple, and gross margin, the way a CFO-turned-VC would. Closes with the IC bear case on unit economics.

Prompt 5: The team risk challenge 🔒 Eight questions about whether your founding team is actually the right one for this specific problem. The hardest category, because it’s personal.

Prompt 6: The why now pressure test 🔒 Seven questions that force a specific, datable argument (not “AI is transforming everything”). Includes the 12-months-too-early test and the trigger reversal scenario.

Prompt 7: The competitive landscape interrogation 🔒 Six questions on whether you truly understand your competitive environment, and whether you’ve named every company an investor will bring up before you do.

Prompt 8: The IC bear case 🔒 Run after all six challenges. Produces the full argument a partner would make to kill your deal in the investment committee, built from your actual weaknesses, not generic ones.

Prompt 9: The pre-meeting sharpener 🔒 15 minutes, the morning of every real meeting. Calibrates your answers for the specific fund, thesis, and investor you’re about to walk in front of.

Prompt 10: The post-meeting debrief 🔒 Six questions to run within 30 minutes of every VC conversation. Across five meetings, the pattern of where you keep going soft becomes impossible to ignore.

All ten prompts, fully written. 50+ additional tools, ready to use today. Seven-day free trial, cancel anytime.

🟦 Prompt 3: The defensibility interrogation

This is the category that has changed most dramatically since 2023. With AI reducing the cost of building almost anything to near-zero, “why can’t a well-funded competitor replicate your product in 12 months?” is now the first question sophisticated investors form, often before you’ve finished your opening slide.

Keep reading with a 7-day free trial

Subscribe to The Founders Corner® to keep reading this post and get 7 days of free access to the full post archives.