10 Questions We Always Ask Founders

After 400+ partner meetings, these are the questions that separate founders who understand their business from founders who think they do.

Most founders prepare for the questions they expect.

The market size. The competitive moat. The go-to-market. They have crisp answers, polished slides, and a narrative that flows. Then we move to the financials, and the room changes.

It is not that founders are hiding anything. It is that most have never been asked to think about their business this way. They know their revenue. They know their ARR. They know their burn. But the questions that matter most go deeper than that, and most founders are not ready for them.

I have sat in over 400 partner meetings across 20 years of investing and building at Notion Capital. The same financial questions come up every single time. Not because we follow a script, but because the answers to these ten questions tell us almost everything we need to know about whether a founder truly understands the machine they are building.

We always start at ten and count down. The further down we go, the harder the questions get.

This is that list. Work through it honestly before your next fundraise. It will save you a lot of pain.

Brought to you by Nume.ai

Most companies don’t die from one big mistake.

They die from numbers they didn’t see.

Burn rises.

Runway shrinks.

Too late.

Nume 3.0 fixes that.

Connect your bank, Xero, QuickBooks.

Nume tracks everything in real time and flags what matters.

Ask → get answers instantly.

Need a forecast or board pack? Nume builds it.

80% faster.

Deeper financial reasoning.

This is what an AI CFO should feel like.

No digging. No delay. No £15K hire.

Try it here with a 14-day free trial, then use code CHRIS50 for 50% off your first month.

Question 10: What Exactly Is Driving Your Growth Right Now?

This sounds like an easy question. It never is.

Most founders answer it with a channel. “LinkedIn.” “Word of mouth.” “Paid search.” That tells me almost nothing. What I am actually asking is: what is the mechanism behind the growth? Is it something you control, something you built, or something that just happened to you?

There is a massive difference between a founder who says “we are growing because we built a referral loop that generates 40% of new signups from existing customers” and a founder who says “we are growing because we got featured in TechCrunch.” One is a business. The other is luck waiting to run out.

Funnels convert users. Loops compound them. The founders who can show me a genuine loop, where one user’s action directly creates the conditions for the next user, are the ones I take seriously.

The founders I trust most can break their growth into three buckets and tell me exactly what percentage comes from each:

Owned growth — referrals, content, SEO, community. Assets you built that compound over time without proportional spend.

Earned growth — partnerships, press, integrations, product-led virality. Growth that comes from doing something well, not from paying for it.

Paid growth — any channel that requires ongoing spend to sustain. The moment you stop paying, the growth stops.

Healthy businesses have all three. But the best businesses have a growing owned engine that reduces their dependence on paid over time. If paid is the only lever, that is a significant concern, because it means your growth is effectively for sale to whoever outbids you.

The answer I am most excited to hear: “Our growth is driven by a product loop we built deliberately. Here is how it works and here is the data that shows it compounding.” That tells me the founder understands their business at a structural level, not just a dashboard level.

Question 9: How Efficient Is Your Growth Engine?

Growth is not valuable in isolation. Growth is only valuable relative to what it costs to produce it.

The metric I use to cut through everything else is the Burn Multiple: net cash burned divided by net new ARR added. It was popularised by David Sacks and it has become, in my view, the single most important efficiency metric for early-stage SaaS.

Below 1x is exceptional. Between 1x and 2x is acceptable. Above 2x is a problem that will get worse, not better, as you scale.

Here is why it matters more than almost any other number: the Burn Multiple captures the whole business, not just one part of it. If you have a CAC problem, it shows up. If you have a churn problem, it shows up. If you have a sales efficiency problem, it shows up. You cannot hide poor unit economics behind strong topline growth when someone is looking at your Burn Multiple.

The LTV:CAC ratio lives alongside it. Healthy is 3:1 or above, meaning the lifetime value of a customer is at least three times what it cost you to acquire them. Below 3:1, you are likely over-investing in acquisition relative to the value being delivered. The payback period matters too: how many months until the revenue from a new customer covers the cost of acquiring them? Under 12 months is good. Under 18 months is acceptable. Much beyond that and your growth is expensive and slow to compound.

Most founders know these numbers in theory. Far fewer track them rigorously and can tell you what is driving changes in them month over month. That is the level of understanding I am looking for.

Question 8: How Durable Is Your Revenue?

Revenue is not all the same. Two companies can both show £100k MRR and have wildly different businesses underneath.

One has 95% of that revenue locked in on annual contracts with strong net revenue retention. The other is on monthly subscriptions with high churn, reactivation campaigns running in the background, and a customer base that is churning faster than the dashboard shows because the churned customers are being replaced with new ones.

The first business is durable. The second is fragile.

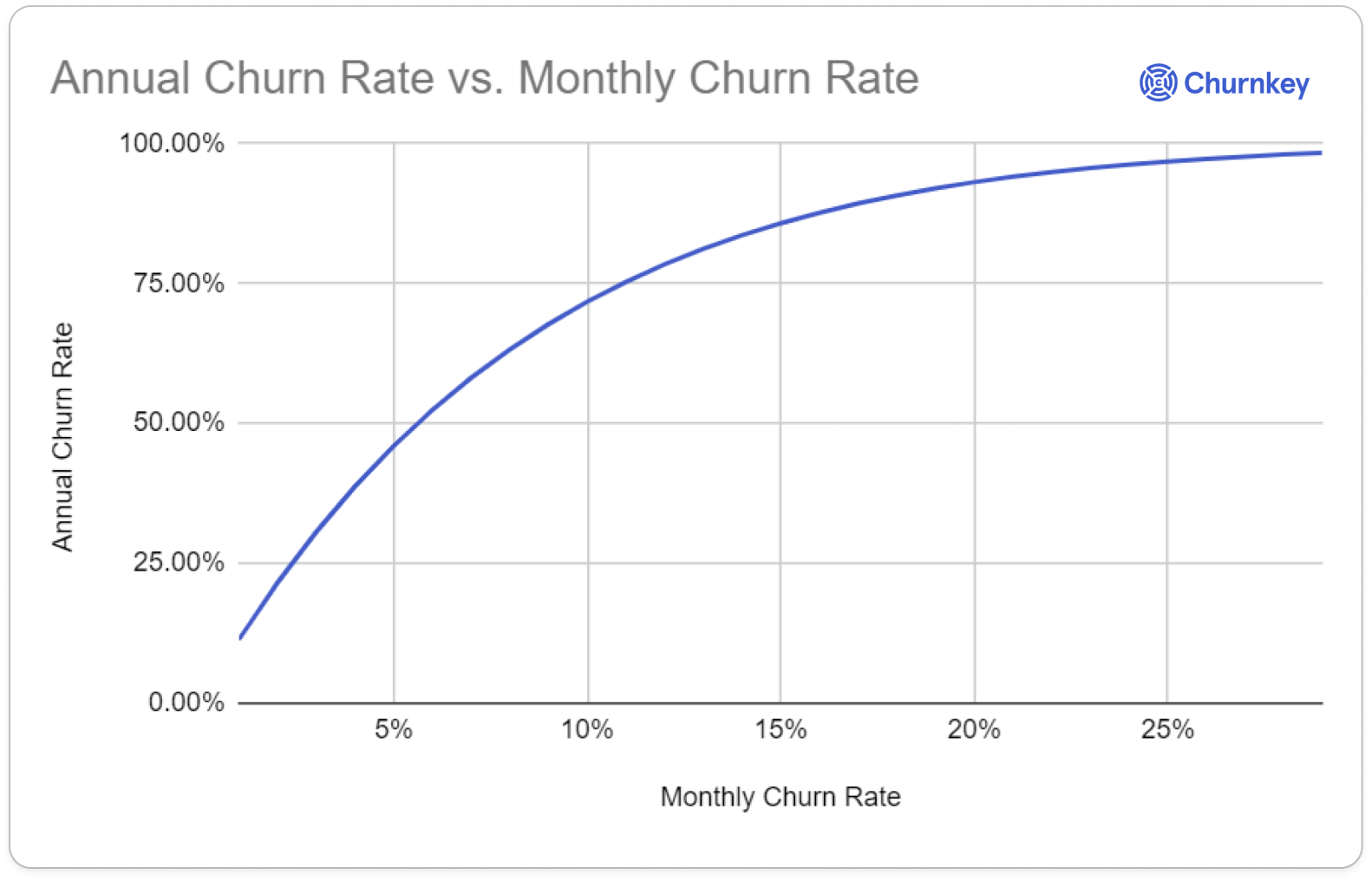

A 2% monthly churn rate sounds manageable. Compounded over 12 months, it means you lose 22% of your revenue base every year just to stand still. Most founders underestimate this completely.

The three numbers I look at to understand revenue durability:

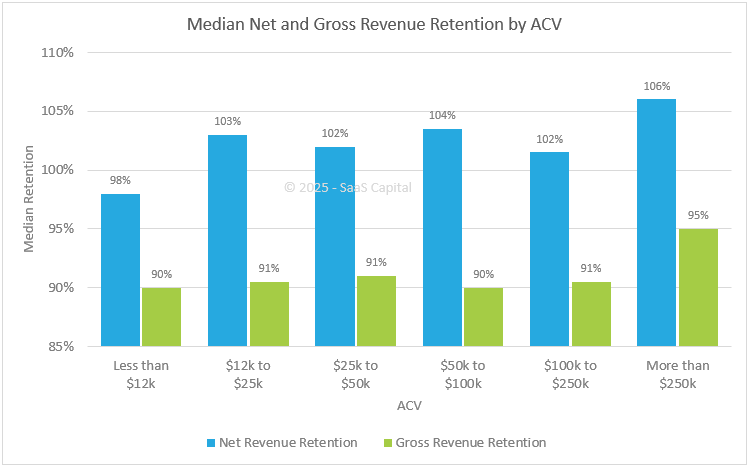

Gross Revenue Retention — of the customers you had at the start of the year, what percentage of their revenue is still there at the end? This strips out any expansion and shows you the raw retention picture. Best-in-class is 90% or above for SMB and 95%+ for mid-market and enterprise.

Net Revenue Retention — now add back expansion, upsells, and cross-sells. If NRR is above 100%, your existing customers are growing faster than they are churning. Above 110% is strong. Above 120% is exceptional and changes the whole economics of the business.

Logo Retention — how many customers do you actually keep? A company can show great NRR while quietly losing a lot of small accounts that are compensated by growth in a handful of large ones. Logo retention tells you whether the business works across the customer base or just for a subset of it.

If I could only look at one number to understand whether a business is genuinely strong or just good at acquisition, it would be NRR. It is the purest signal of product value, customer success, and pricing architecture working together. Mediocre products with great sales teams can acquire. Only genuinely good products retain and expand.

Question 7: Where Exactly Are You Losing Customers, and Why?

Churn is rarely uniform. That is the thing most founders miss.

When I ask this question, what I am really asking is: have you done the work to understand your churn at a cohort level? Because aggregate churn numbers are almost always misleading. They mix very different customer behaviours into a single number that makes the business look either better or worse than it actually is.

The colour shading makes it immediately visible. Green is retention. Red is churn. The moment you see this chart, aggregate numbers become useless. You stop asking “what is our churn rate?” and start asking “what happened to the August cohort in month two?” That is the right question.

The cohort analysis is what changes everything. When you break churn down by acquisition month, channel, company size, industry, and product tier, patterns emerge that are completely invisible in aggregate. A founder who can tell me “our highest churn is in SMB customers acquired through paid search who never completed onboarding in week one, and that cohort is only 15% of our revenue” has a very different business from a founder who says “our churn is 3% monthly across the board.”

Here is how I want founders to think about diagnosing churn:

Time to value. When do customers who eventually churn first show signs of disengagement? In most SaaS businesses, the customers who churn in month six showed low engagement signals in week two. If you can identify those signals early and intervene, churn becomes a product problem to be solved, not just a number to be managed.

The exit interview. Most companies do not do these rigorously. The ones that do find that “too expensive” almost never means the product cost too much. It usually means the perceived value did not justify the price, which is a completely different problem with a completely different solution.

The silent churners. Customers who cancel and tell you why are doing you a favour. The dangerous ones are the customers who just stop engaging and eventually let the subscription lapse. Building product signals that identify these customers before the cancellation moment is one of the highest-leverage things a product team can do.

The founder who cannot tell me specifically where they are losing customers and why has not done this work. That is fine, but it means they do not fully understand their business yet.

Question 6: What Does Your Growth Look Like at the Current Pace?

This is not a question about ambition. It is a question about ceiling.

Every business has a current growth mechanism, and every growth mechanism has a natural limit. The question is whether the founder has thought about where the ceiling is, and what happens when they hit it.

I have seen this play out so many times. A founder scales a paid channel brilliantly, gets to £2M ARR, and then discovers that the audience they were targeting on that channel is exhausted. CPAs start climbing. Conversion rates fall. The mechanism that got them here stops working. And they have not built the next engine yet.

Your current beachhead is not your final market. But each outer circle requires a deliberate new motion to unlock. Assuming the next circle opens automatically when the first one is won is one of the most expensive mistakes a founder can make.

The version of this question I find most revealing is: if you double the money going into your current growth motion, what happens?

If the answer is “our revenue roughly doubles,” the engine is genuinely scalable and we should talk seriously about putting more capital in. If the answer is “it gets more expensive and probably delivers diminishing returns,” then you need a second engine before you raise, because this round will not achieve what you are projecting.

The best founders have thought about the natural size of their current market, identified where the ceiling is, and have a specific plan for what growth motion they will build next. They are not waiting until the ceiling arrives to start planning. They are building the next engine while the current one still has fuel.

Question 5: What Happens to Your Unit Economics If Growth Slows?

Growth flatters everything. It is one of the things I have learned most clearly from watching hundreds of businesses through cycles.

When you are growing fast, the new revenue covers the cracks. Customer success problems get papered over by acquisition. Churn gets hidden by replacement. Pricing weakness gets masked by volume. The moment growth slows, even temporarily, all of those issues become visible at once.

I ask this question to understand whether the business model itself is sound, or whether it only works above a certain growth rate.

The most common startup killer is cash depletion. In most cases, a growth slowdown is what exposed the problem, not the slowdown itself. The underlying issue was structural and the growth rate was masking it.

The specific thing I am probing for is this: if you grew at half your current rate for six months, what breaks first? Does the unit economics still work? Can you hit profitability at that growth rate, or does the business only work at current or higher velocity?

There is no right or wrong answer to this. Fast-growing businesses often genuinely need a certain growth rate to justify their cost base, and that is fine if the trajectory is clear and the funding to sustain it is secured. What is not fine is a founder who has not modelled this scenario and has no idea what breaks first.

The businesses I back have founders who can answer this question with specifics. “At half our current growth rate, our payback period extends from 10 months to 18 months, and we would need to reduce our sales team headcount plan by three people to maintain runway to our next milestone.” That kind of clarity does not happen by accident. It comes from doing the work.

Question 4: How Predictable Is Your Revenue?

Predictability is underrated. It is also one of the things investors value most highly, even when founders do not realise it.

A business with £500k ARR growing unpredictably is harder to fund than a business with £300k ARR growing reliably. Because predictability tells me that the underlying mechanism is understood, that the inputs and outputs have a consistent relationship, and that the projections you are showing me have a reasonable chance of being accurate.

This is the matrix investors are running in their heads when they evaluate your business. High NRR and low CAC payback compound together. Either number in isolation is interesting. Both together in the top-right quadrant is fundable at a premium valuation.

The specific things that build revenue predictability:

Annual contracts. Monthly subscriptions are convenient for customers but terrible for business predictability. Every month is a renewal decision. Annual contracts lock in revenue for 12 months, dramatically smooth your cash flow, and allow you to plan headcount and investment with confidence. I always ask what percentage of revenue is on annual versus monthly, and what is the trend.

A pipeline that moves consistently. If your sales cycle has a reliable 60-day conversion rate and a consistent average contract value, your next quarter’s revenue is largely visible in your current pipeline. If deals are lumpy, highly variable in size, or unpredictable in close timing, your revenue is unpredictable by definition.

Expansion revenue from existing customers. This is the most predictable revenue of all, because it comes from customers you already understand. Companies with strong expansion motions — seat expansion, usage growth, product upsell — have a much smoother revenue curve than companies that depend entirely on new logo acquisition.

The founder who cannot tell me their pipeline coverage ratio for next quarter and their confidence interval around their monthly targets has not yet built a predictable business. That does not mean I will not invest, but it shapes how I think about the risk and the capital required.

🔒 The 3 Most Important Questions We Ask

Before committing to a GTM motion, there are three questions we always ask.

They’re simple on the surface.

But they force a level of clarity most founders never get to.

Because the numbers can look good.

Revenue growing. Deals closing. Pipeline building.

And still, underneath it all, the economics don’t work.

These three questions are designed to cut through that.

The first anchors you in what you can actually afford to spend.

The second shows you what you’re really spending to acquire a customer.

And the third is where it all comes together.

It’s the one that makes it impossible to ignore whether the motion is viable or fundamentally broken.

If you’re about to hire, increase budget, or double down on growth, you need to run this first.

Keep reading with a 7-day free trial

Subscribe to The Founders Corner® to keep reading this post and get 7 days of free access to the full post archives.